BRITAIN’S GROWTH TRAP

Born here, Grown elsewhere

THE GROWTH TRAP: A TLDR FOR PEOPLE WHO READ THE LAST PAGE FIRST

Billionaires are not the problem. They are the mechanism.

Britain has spent twenty-five years treating technology billionaires as a distributional failure. The data says the opposite.

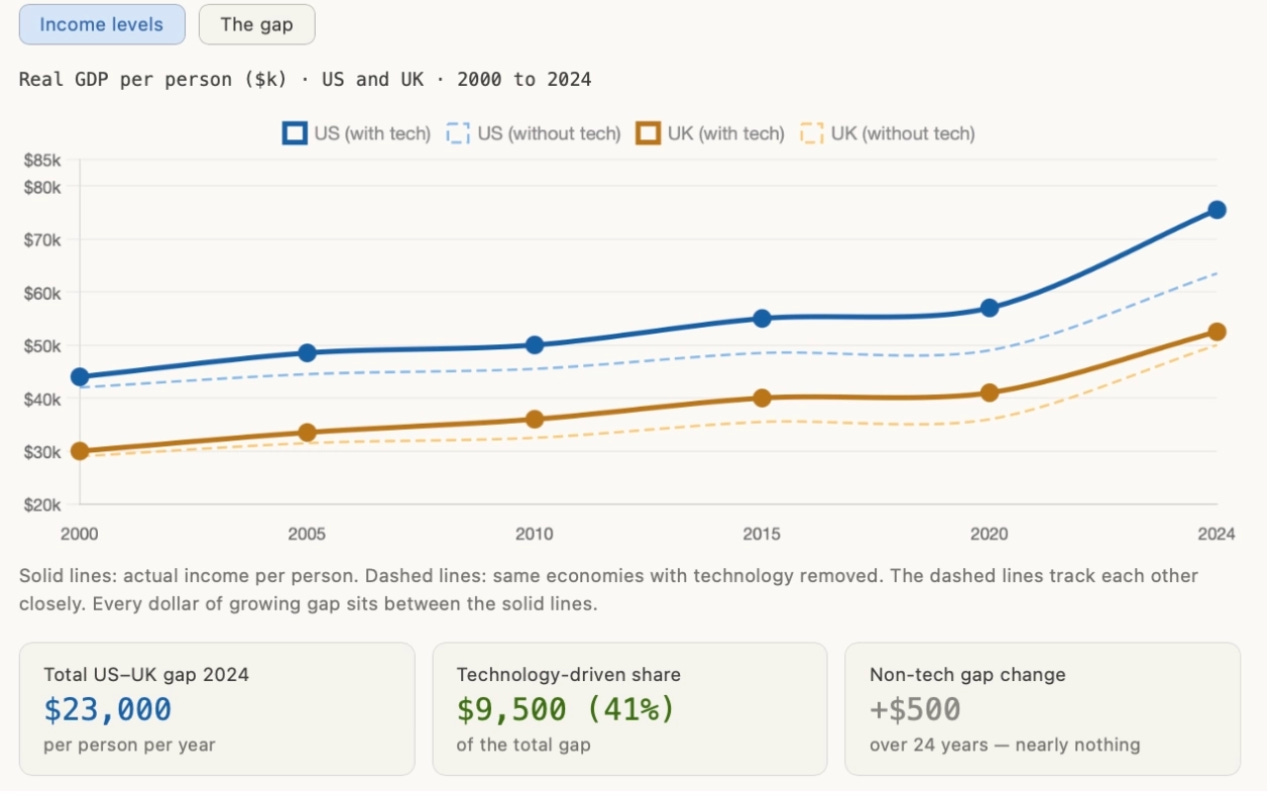

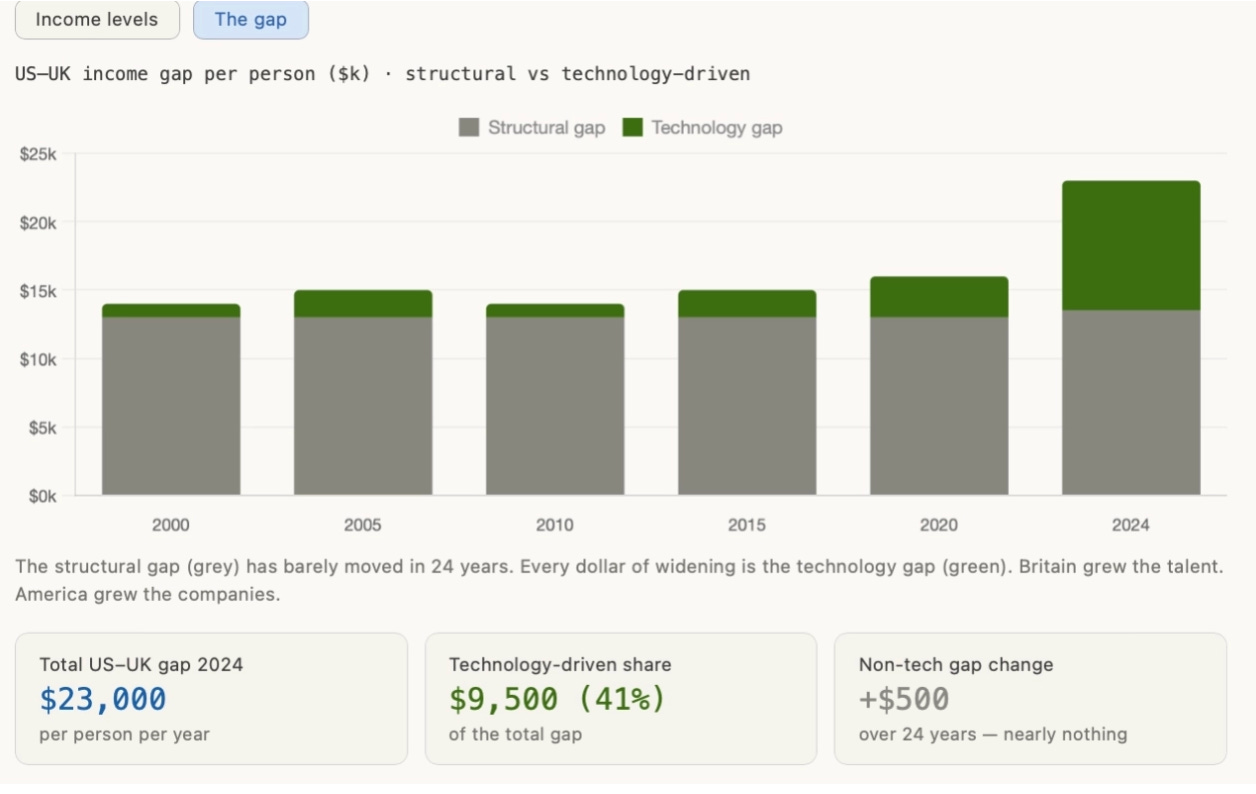

Start with the number that should settle the argument. Strip technology out of both economies and compare American income per person with British income per person over the last twenty-four years. The structural gap has moved by roughly five hundred dollars. Per year, that rounds to nothing. The entire additional widening - roughly nine thousand dollars of extra annual income per person - came from one place. Not from harder-working Americans. Not from lower wages or weaker unions. From a single recycling loop that turned a £1.2 billion technology exit in 2002 into an ecosystem worth six trillion dollars today. Strip out the EU’s technology sector and the same flatness holds there too. The gap between all three economies and GDP per capita, once you remove technology, has barely moved in a generation.

That loop worked because of a specific mechanism. When PayPal was sold in 2002, the people who built it walked out with capital and hard-won operational knowledge simultaneously. They recycled both into the next generation of companies. Those founders recycled into the generation after. Each cycle started from a richer base than the last because the knowledge compounded alongside the capital. Britain watched every generation of that loop from the outside.

What Britain keeps losing is not abstract. It loses companies: DeepMind, sold to Google. ARM, sold to SoftBank, listed in New York. Graphcore, sold below its fundraising total. Autonomy, sold to Hewlett-Packard. Revolut, worth more than Barclays, being lobbied to consider London as a secondary option for a company it built here. Improbable, $3.4 billion, Cambridge. Herman Narula, Dubai, November 2025. The specifics differ. The direction has never changed. It also loses people: Britain had the biggest net drain of millionaires of any country in 2025.

The argument that Britain should have fewer of these people rests on a misreading of what founders actually keep. When Jeff Bezos stepped back as chief executive of Amazon he owned under ten percent of the company. More than thirty percentage points of what is now worth two and a half trillion dollars had been distributed outward - to pension holders, to staff through share awards, to the investors who funded every stage of growth. He built it. He kept a fraction. The same pattern holds everywhere. Founders keep a small slice of the equity. The equity itself is a fraction of total value created - wages, customer savings, tax revenues, and the ecosystem their exits seed all sit outside it entirely.

The argument that this is too much is an argument for generating less of what flows to everyone else.

Britain cannot redistribute its way out of a compounding gap.

This is what each chapter sets out to prove.

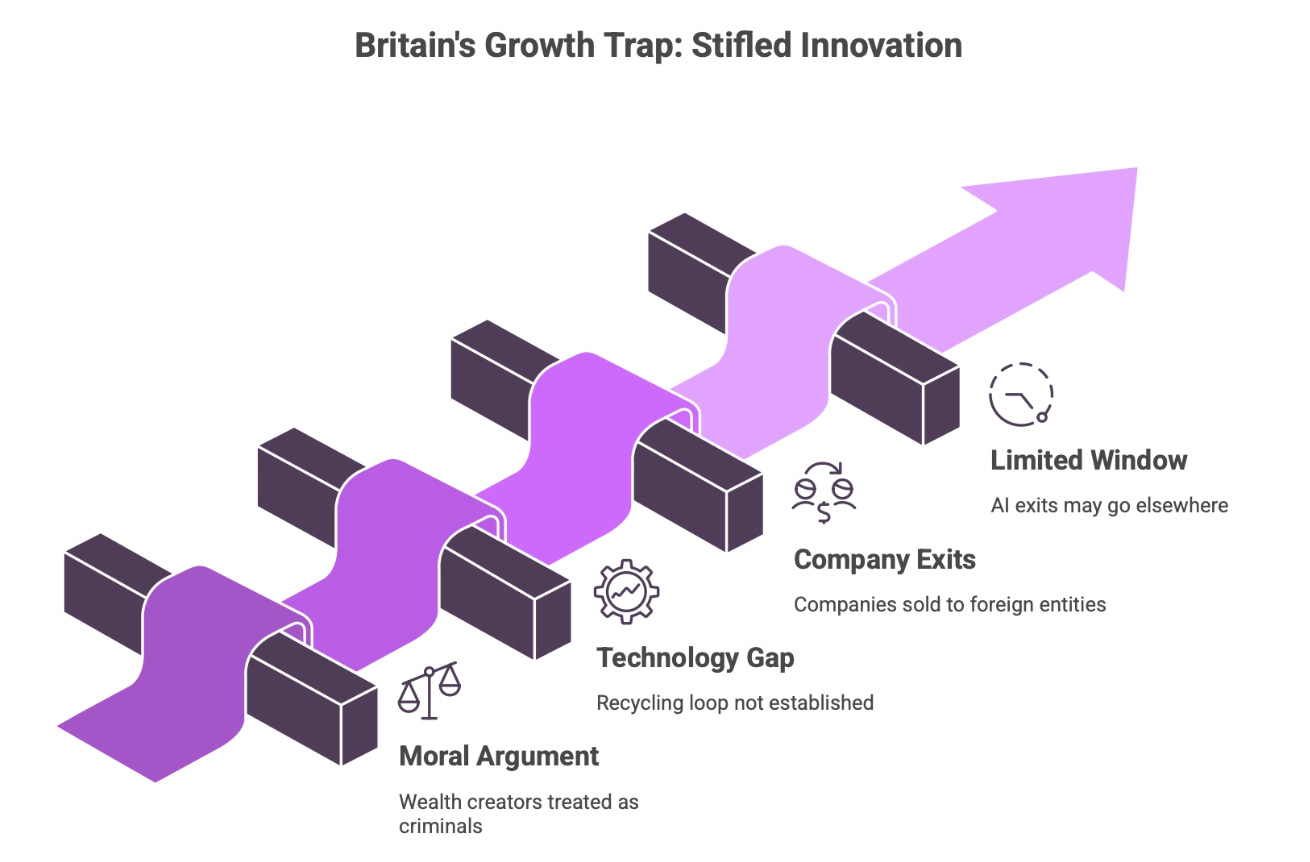

Chapter one: Britain has built a moral argument that treats wealth creators like criminals. It feels righteous. In 2025 it lost more millionaires than any other country on earth. The data shows this moral posture has been making ordinary people poorer for twenty-five years.

Chapter two: Strip out technology and the structural gap in GDP per capita between Britain, America, and Europe has not widened in twenty-five years. Every dollar of additional divergence is explained by a single recycling loop in which each generation of American founders seeded the next with capital and hard-won knowledge. Britain watched it being built. Then spent a generation stopping it from running here.

Chapter three: Britain has lost DeepMind, ARM, Graphcore, and Autonomy, and now risks losing Revolut. The definition of insanity is doing the same thing repeatedly and expecting a different result. Britain has been doing it for thirty years.

Chapter four: Britain has a five-year window to decide whether its first AI exits seed the next generation here or in California. The opportunity is real. The window is not permanent.

CHAPTER ONE

Britain’s Favourite Moral Argument Is Making Ordinary People Poorer

‘It is only fair that those with the broadest shoulders should bear the greatest burden’ is the most unchallengeable sentence in British politics. It has also done more damage to ordinary British living standards than any other idea of the last twenty-five years.

Fairness matters. But the specific policies Britain has built around this principle, applied with particular force to technology wealth, have been producing the precise opposite of fairness for a generation. This chapter is the proof.

The number

The number appeared in the summary. Here is what it means for the fairness argument. Strip technology from both economies and the gap in living standards between America and Britain has barely moved in twenty-four years. The entire additional widening - roughly nine thousand dollars of extra annual income per person - came from a single recycling loop that Britain watched being built in California and then spent two decades actively preventing from being replicated here. A policy framework that extracts from exits rather than compounding them has been choosing, year after year, to keep that gap exactly where it is. This is not a conservative argument or a libertarian one. It is what the data says.

What the culture produces

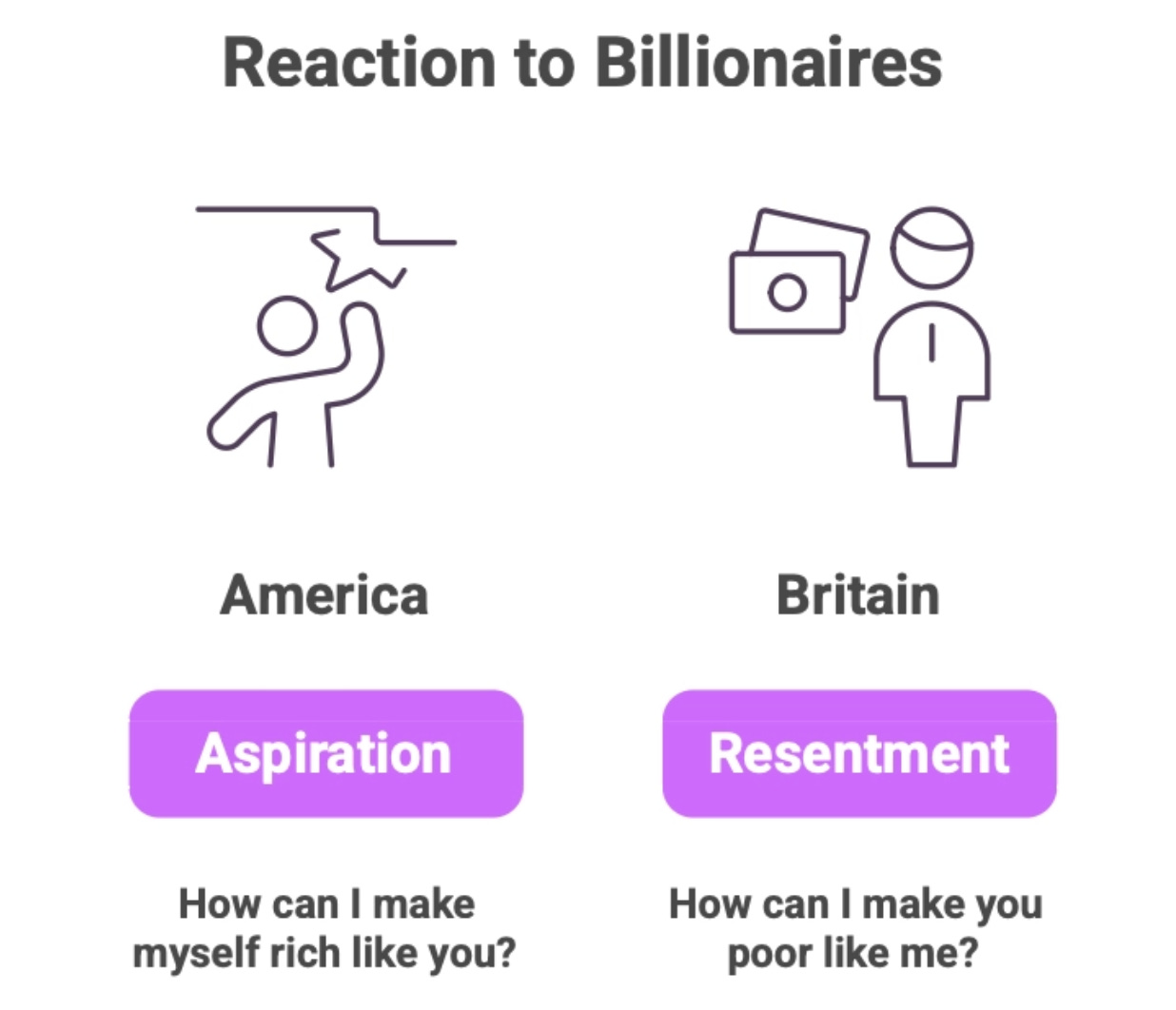

In America, when someone builds a company worth a billion dollars, the reaction of the average person and the average newspaper is roughly this: how did they do that, and how do I get there? The billionaire is evidence that the system works, a signal about what is possible.

In Britain, when the same thing happens, the reaction is roughly this: how much of that can we take? The billionaire is evidence that the system has failed, a problem to be redistributed, a story about luck and privilege and what someone owes.

One culture compounds. The other extracts. In Britain, founder wealth is treated as presumptively suspect. That suspicion is not just a feeling. It is encoded in policy that shifts with every budget, which breaks the long-horizon bets that compound loops require. The gap in the chart is what those two dynamics produce over twenty-five years. Both jaws of the trap must open simultaneously for the escape to work.

In 2025, Britain lost more millionaires than any other country on earth. Over sixteen thousand people with investable assets above a million pounds either left or were counted as departed. Britain is the only one of the world’s ten wealthiest countries whose millionaire population has shrunk over the past decade, while the United States grew its by seventy-eight percent.

Founders keep a fraction. Everyone else gets the rest.

Before the broadest shoulders argument continues to dominate British policy unchallenged, it is worth looking honestly at what founders actually keep when they build something of real scale. The numbers operate on two levels. Founders own a shrinking percentage of the equity they create - diluted by investor rounds, staff share schemes, and secondary sales. And equity itself captures only a fraction of total value created: wages, customer savings, supplier profits, tax revenues, and the ecosystem seeded by the exit all sit outside it. Put both layers together and the founder’s actual share of everything their company generates runs between one and three percent. Customer savings and spillovers are hard to measure precisely, but the direction is unambiguous: the equity slice is small relative to the total surplus a scaled company throws off. The rest belongs to everyone else.

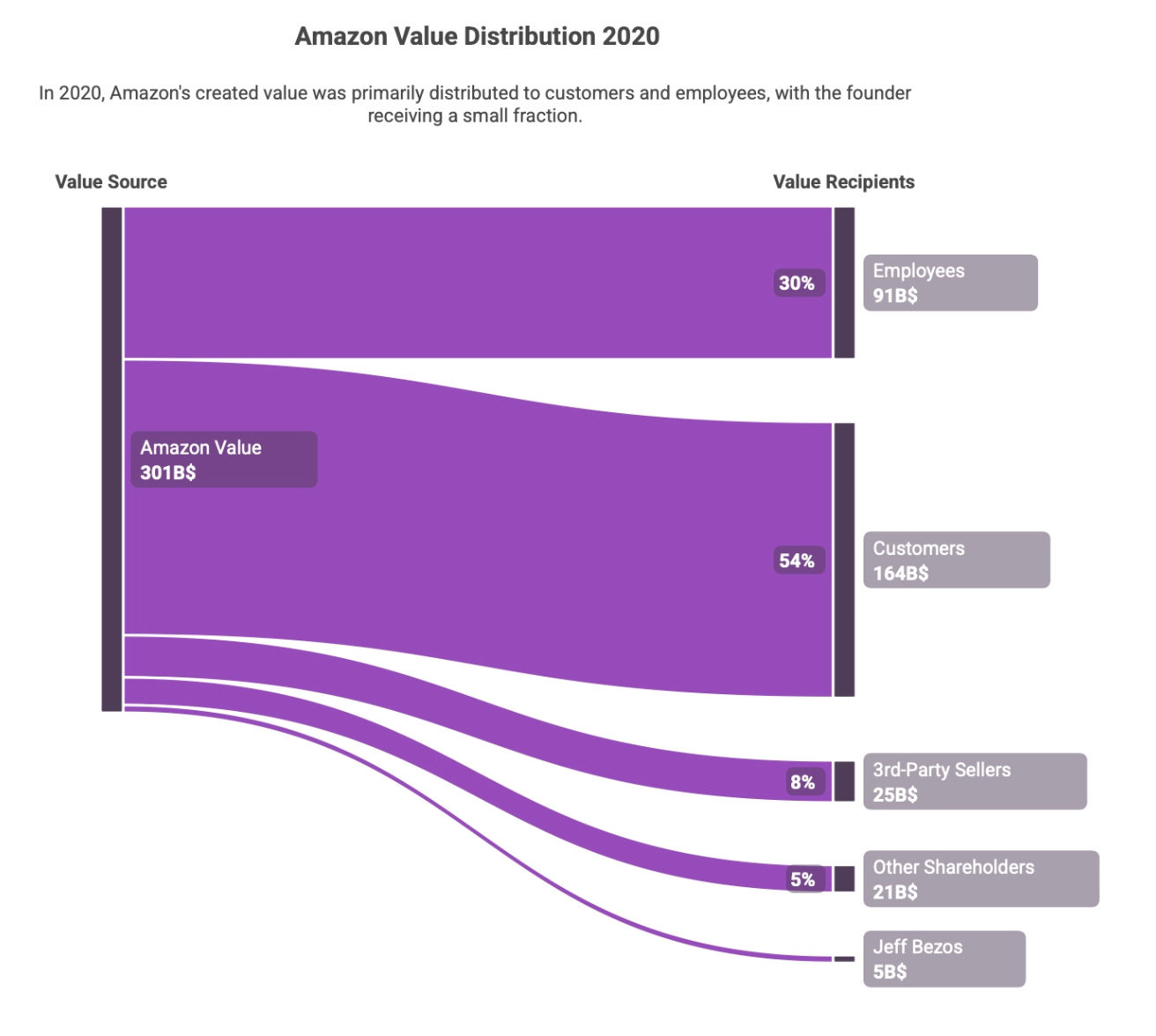

In 2020, Jeff Bezos calculated where all the value Amazon created that year went. Employees received $91 billion in wages and benefits. Customers saved roughly $164 billion through lower prices. Third-party sellers made $25 billion in profit through the platform. Shareholders received $21 billion. Bezos personally received about one and a half percent of total value created. One and a half percent. When Amazon listed in 1997, he owned forty-three percent. When he stepped back as chief executive, he owned under ten percent. He built it. He kept a fraction.

Mike Lynch’s numbers tell the same story at a British scale. He built Autonomy, sold it for eleven billion dollars, kept approximately seven percent. The portion he kept he recycled into Darktrace and a generation of Cambridge technology companies. One founder, one exit, one reinvestment cycle, and the British AI ecosystem is measurably better for the companies it produced.

The argument that Britain should have fewer of these people is an argument that Britain should generate less of the ninety-seven to ninety-nine percent that goes to everyone else. It is not a fairness argument. It is a poverty argument dressed in the language of fairness.

What the policy produced

Founders who build companies to real scale face capital gains tax of 24% on gains above the first million pounds, with the preferential founder rate under Business Asset Disposal Relief having risen from 10% to 18% by April 2026, while economists continue to lobby for full alignment with income tax rates that would push it towards 45%. The direction is unmistakable even if the worst has not yet arrived. The policy framework has consistently chosen to extract revenue from the moment of wealth creation rather than keep that wealth inside the country where it can compound into the next company. In each case the founders paid their taxes, the state received its share, and the knowledge those founders had accumulated left the country along with the exit proceeds.

Britain is not being offered a choice between fairness and technology wealth. It is being offered a choice between two kinds of unfairness. The first is the unfairness of concentrated technology wealth inside Britain, addressable through progressive taxation on consumption and assets rather than on the act of building companies, through housing policy and public investment funded by a growing tax base. The second is the unfairness of a Britain that stays on the slow flat growth line while America compounds - a Britain in which the care worker, the teacher, the construction worker, fall further behind their American counterparts every year. Not because of anything a technology billionaire did to them, but because the growth that a domestic compound loop would have generated never happened here.

Britain has been choosing the second unfairness while believing it was choosing against the first.

The nine thousand dollars per person per year that Britain is not generating compared to America is not an abstraction. It is the nurse who cannot afford to buy a house in the town where she works. It is the NHS waiting list that a richer tax base could have shortened.

The second chapter explains how this recycling loop works and why Britain, by failing to build it, has been subsidising American prosperity with its own talent.

CHAPTER TWO

The Recycling Machine: Why Britain Is Paying for American Prosperity

In the year 2000, the gap in income per person between the United States and the United Kingdom was approximately fourteen thousand dollars. (All figures in this article use purchasing power parity adjusted dollars, which account for differences in the cost of living between countries. When a British figure appears in pounds it is noted explicitly. Otherwise assume dollars throughout.) In 2024 that gap is twenty-three thousand dollars. Nine thousand additional dollars of annual income per person, built up over a single generation, separating two countries that share a language, a legal tradition, broadly similar education systems, and outside of technology, broadly comparable economies.

Strip technology out of all three economies and recalculate. The structural gap in GDP per capita between the US, the UK, and the EU has barely moved in twenty-four years. The non-technology divergence is flat across all three. The technology gap is everything.

If American structural advantages were driving the divergence independently of technology, those advantages would be lifting American non-technology sectors above their British and European equivalents at a comparable rate. They are not. The structural gap has been stable. The growing gap is a different story. The PayPal alumni and their subsequent recycling cycles provide a specific explanation with unusual precision.

The two reasons America pulled away

The US technology sector outgrew every comparable economy for two reasons. The first is cultural: a society that celebrates wealth creation rather than resenting it produces more of it. In America, when someone becomes a billionaire, the average person’s reaction is: how did they do that, and how do I get there? In Britain, the reaction is: how much of that can we take? One culture compounds. The other extracts. In Britain, founder wealth is treated as presumptively suspect. That suspicion is encoded in policy that shifts with every budget, which breaks the long-horizon bets that compound loops require.

The second is mechanical: a recycling loop in which each generation of founders seeded the next with capital and hard-won knowledge, compounding value across four generations. The mechanical reason is the one Britain can copy without waiting for a cultural revolution.

The mechanism

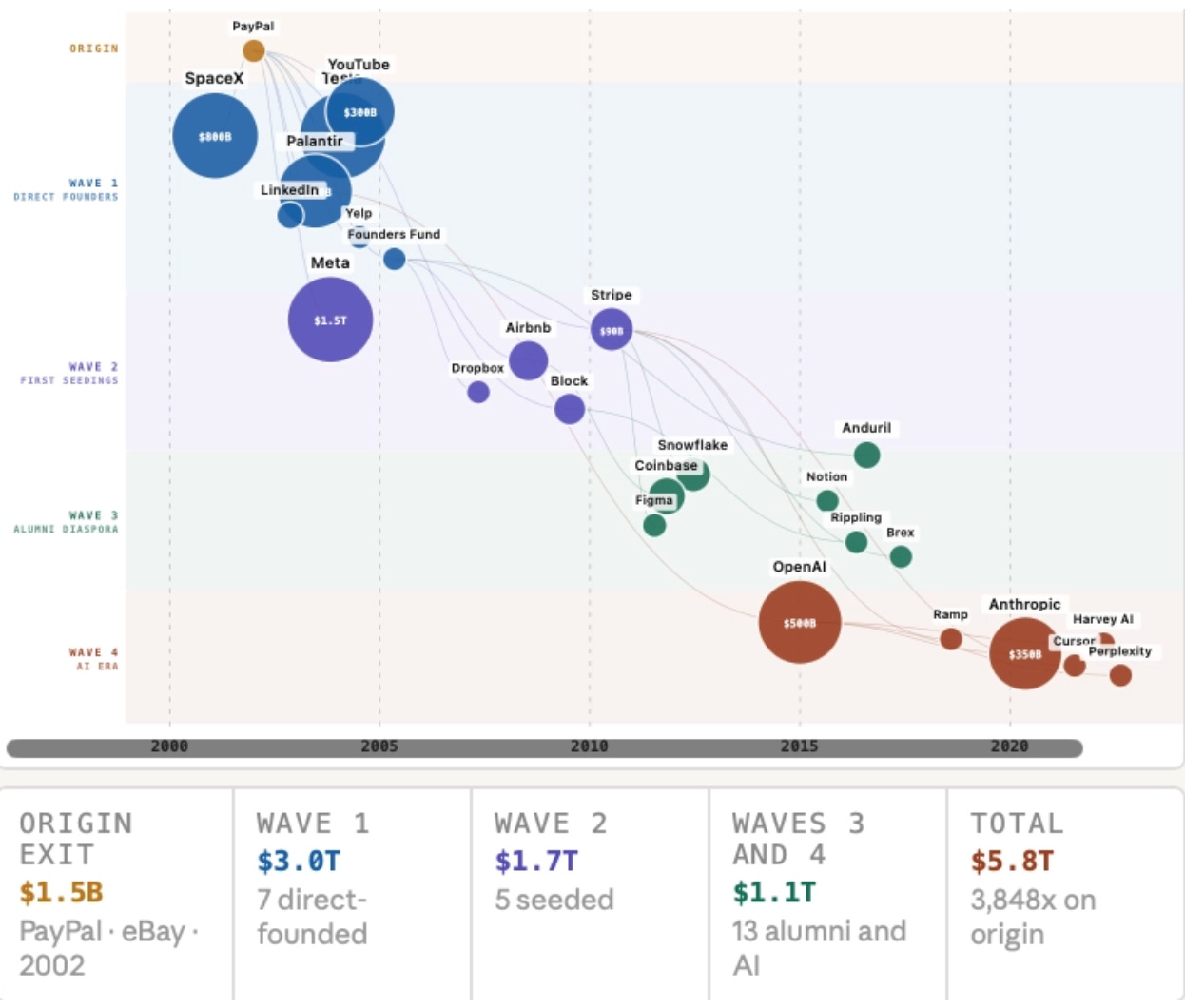

In October 2002, eBay acquired PayPal for $1.5 billion. Approximately two hundred and twenty people walked out of that transaction with something that does not appear on a balance sheet: a library of hard-won knowledge accumulated through building a payments system at scale, surviving the dot-com crash, and learning what it actually feels like when a product grows faster than anyone expected.

Peter Thiel owned roughly 3.7 percent. Within two years he had invested five hundred thousand dollars of his exit in a twenty-year-old’s social network. He did not just bring money. He brought the specific knowledge library built at PayPal: what the early stages of a platform business actually require, how real identity works differently from avatar-based networking, when to resist investor pressure and when to accept it. His $500,000 became over a billion dollars. He used that to found Founders Fund, which invested in SpaceX, Airbnb, Palantir, Stripe, and dozens of others. Elon Musk took his share and built Tesla and SpaceX simultaneously. Reid Hoffman founded LinkedIn, then became one of the earliest and most consequential investors in the companies that followed.

None of this was charitable. It was commercially motivated recycling of capital and knowledge. The total effect of two hundred and twenty people doing versions of this simultaneously, across a decade, with each generation starting from a richer knowledge base than the last, is what produced the gap in the chart.

There is a name for the kind of knowledge that made this loop so powerful. A Xeme (more in my Xeme Framework) is the smallest unit of real-world learning, earned through doing something at scale and understanding from direct experience why it worked or failed. It is not what you learn from a lecture or a case study. It is what you carry after you have lived through something difficult at scale. When the PayPal group recycled their exits, they recycled both capital and xemes simultaneously. The Stripe founders who started Brex, Ramp, and Rippling began with Stripe’s full knowledge library available to them. The OpenAI alumni who founded Anthropic started with everything the preceding three generations had learned.

The key variable distinguishing the three economies is recycling density: the concentration of accumulated operational knowledge that stays inside a country’s borders, recycles freely into the next generation of domestic founders, and grows with each cycle. The United States has the highest recycling density of any technology ecosystem in the world. Britain’s recycling density in artificial intelligence is close to zero. Not because the knowledge does not exist here, but because the mechanism that would keep it here has not been allowed to develop.

Mario Draghi’s 2024 report on European competitiveness reached the same conclusion from a different angle. No European company worth more than a hundred billion euros has been founded from scratch in fifty years. Thirty percent of European startups valued above a billion dollars moved headquarters abroad between 2008 and 2021. In the five years to mid-2024, worker productivity per hour in the eurozone rose by 0.9 percent. In the United States it rose by 6.7 percent. Britain is running the same experiment as the EU with the same results.

The most technically serious objection is that American structural advantages - a single domestic market of three hundred and thirty million people, immigration designed to bring in exceptional talent, deeper capital markets - could plausibly explain the divergence independently. The structural advantages are real but they explain the existing gap, which has been stable for twenty-four years. They do not explain the nine thousand dollars of additional widening that opened up on top of it.

The third chapter counts the cost in specific companies and specific people, and asks whether Britain can still understand what it keeps losing before the next generation of exits follows the same path.

CHAPTER THREE

Britain’s Most Expensive Misunderstanding

Barney Hussey-Yeo founded Cleo in London in 2016. He was twenty-four years old, working from his bedroom in Shoreditch, building an AI-powered financial assistant for people who struggled to manage money. By 2018 he had raised serious capital. By 2020 he had moved the company entirely to the United States. Not because Cleo failed in Britain. Because the conditions that would have let it grow to the scale he had in mind did not exist here. In November 2024, standing at the sidelines of a fintech conference in London - still physically present, still a British founder - he told CNBC: “There’s so many founders already leaving, or already considering leaving - and they’re excited to go to Silicon Valley.” The excitement about Silicon Valley was not his. It was everyone around him.

He subsequently gave evidence to the House of Lords Communications and Digital Committee. What he said was not a complaint. It was a structural diagnosis. “There is now a ceiling on what the most ambitious founders can achieve here. A shortage of growth-stage capital, an onerous regulatory environment and a broken London Stock Exchange leave virtually no path to scale or list generational companies domestically.” He wrote in Fortune the same week: “Moving to America went beyond market size - it was a stark recognition that Britain stifles ambitious tech companies.”

Hussey-Yeo is the pattern.

The roll call

The specifics of each departure below differ. Some were acquisitions. Some were listings. Some were founders who left. The direction is unbroken.

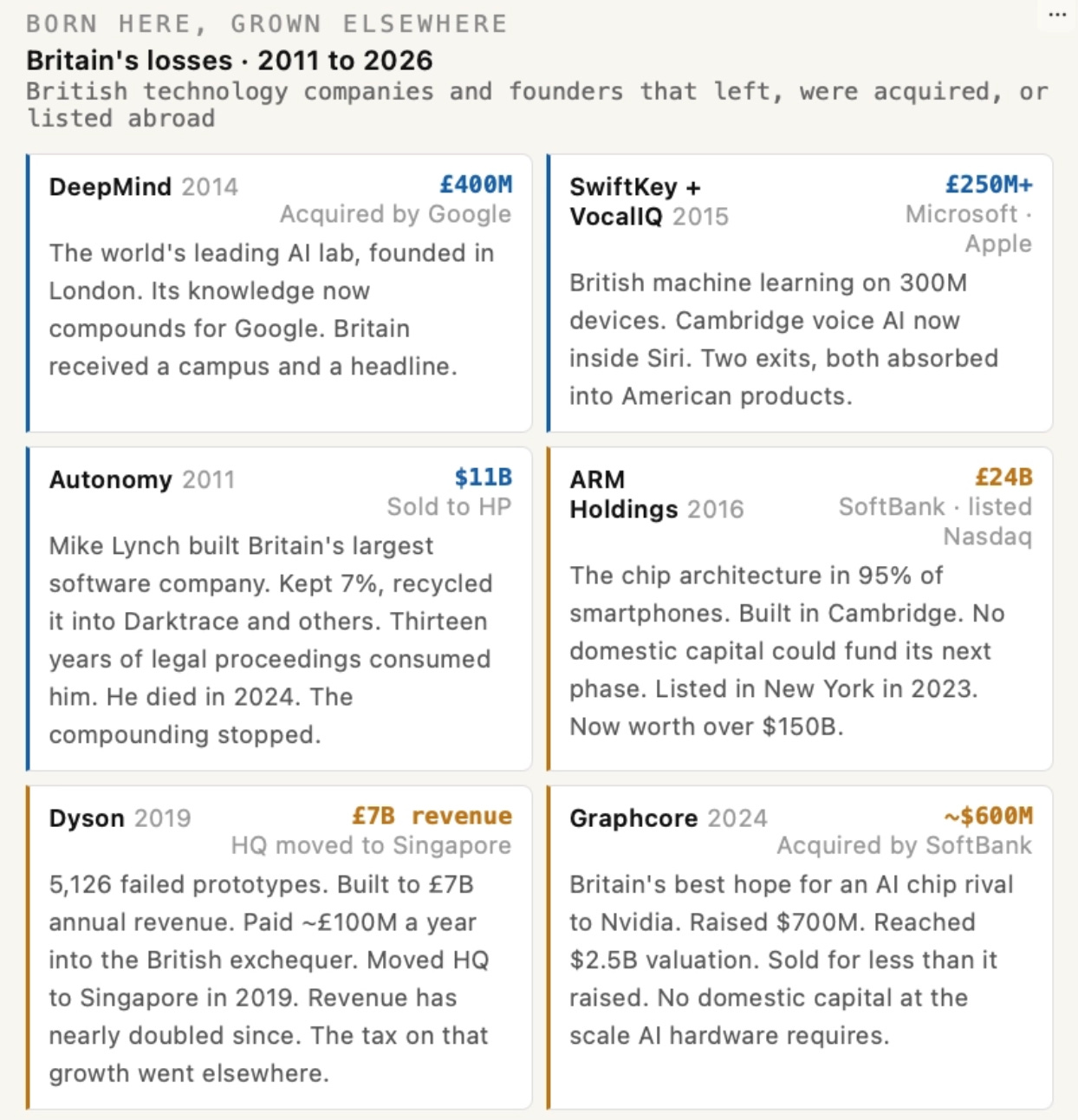

In 2014, Google acquired DeepMind, founded in London, for approximately £400 million. The founders’ accumulated knowledge of how to build AI research at the frontier went into Google’s product organisation, where it has been compounding for American national income ever since. Britain received a campus and a headline.

In 2016, Microsoft acquired SwiftKey, whose machine learning technology sat on over three hundred million devices. The same year, Apple acquired VocalIQ out of Cambridge, voice AI that now lives inside Siri. Both generated the same pattern: British talent, British research, British operational knowledge, transferred to American balance sheets.

ARM is the wound that does not close. Founded in Cambridge, the company designed the chip architecture inside ninety-five percent of the world’s smartphones. In 2016, with no domestic capital source capable of funding its next phase of growth, the government approved its sale to SoftBank for £24 billion. Ministers called it proof that Britain remained open for business. Seven years later ARM chose Nasdaq, not London. The company that should have anchored a British semiconductor ecosystem trades in New York at a valuation above $150 billion.

Hermann Hauser co-founded Acorn Computers in Cambridge and spun out ARM in 1990. He had voted against the SoftBank sale. When the Nvidia acquisition bid came in 2020 he warned publicly that it would result in Britain having to ask the President of the United States for permission to use its own Cambridge-designed microprocessors. He described British politicians as “technologically illiterate” and the “root cause” of the problem. He has been saying this for thirty years. The company he built has changed hands twice. His argument has not changed once.

Graphcore should have been Britain’s Nvidia. Founded in Bristol in 2016, backed by Microsoft, Sequoia, and by Demis Hassabis as a personal investor, it raised $700 million and reached a $2.5 billion valuation. Then it ran out of runway because no domestic source of capital could fund the scale the AI hardware market required. In 2024 it was acquired for an estimated $600 million, below the total it had raised.

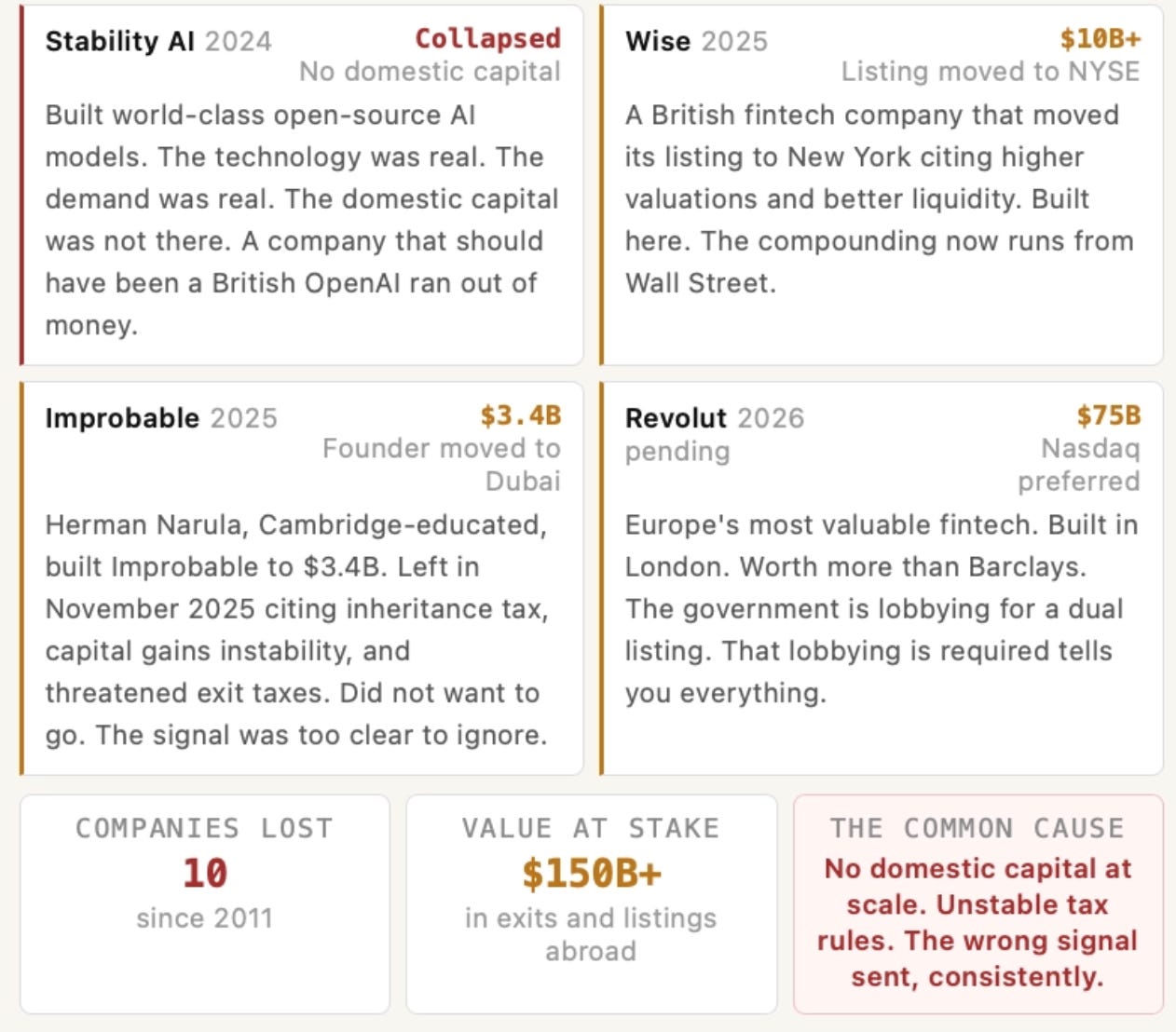

Stability AI ran out of money. The technology was real. The demand was real. The capital was not there.

Mike Lynch built Autonomy from a Cambridge laboratory into Britain’s largest software company and sold it to Hewlett-Packard for $11 billion in 2011. He put a portion into Invoke Capital, which was one of the first investors in Darktrace in 2013. One successful British founder, recycling one exit into many companies, exactly as the mechanism in the second chapter predicts. Then thirteen years of legal proceedings consumed him. He died in August 2024. The recycling stopped.

Darktrace is the proof that the mechanism works when conditions allow it to run. Lynch seeded it in 2013. It grew to employ over two thousand four hundred people, generated £625 million in annual revenue by 2024, and became one of the world’s leading AI cybersecurity platforms. One founder, one exit, one reinvestment cycle. The Lynch-Darktrace loop is exactly what this article is arguing for. It is also the clearest possible illustration of why the loop cannot depend on a single person. Lynch died and the compounding stopped. Darktrace has since been taken private by American firm Thoma Bravo. Britain needs a cohort, not a hero.

Revolut: built in London from 2015, sixty-five million customers, $4 billion in revenue in 2024, pre-tax profit of $1.4 billion, worth more than Barclays at $75 billion. Its chief executive has said publicly that the company prefers a US listing over London. The government is lobbying for a dual listing. The fact that lobbying is required tells you everything about the signal Britain has spent decades sending.

Herman Narula learnt to code at twelve, studied at Cambridge, co-founded Improbable at twenty-nine. The company became worth $3.4 billion. Before he left for Dubai in November 2025 he gave an interview to The National. “It’s less about the exit tax and more about not knowing what the next five budgets are going to hold and what random things are going to be placed inside them,” he said. “This is a country that was the birth of the Industrial Revolution, and now it doesn’t even have a single domestic company of note associated with AI.” He did not want to leave. He said so plainly: “I don’t particularly want to leave the UK - but I might want to one day and I don’t want to be banned from that option.”

What follows is not a list of companies that could not make it. It is a list of companies that did.

Born here. Grown elsewhere.

DeepMind. ARM. Graphcore. Autonomy. SwiftKey. Stability AI. Wise choosing New York. Revolut being lobbied to consider London as a secondary option. Improbable, $3.4 billion, Cambridge. Herman Narula, Dubai, November 2025.

Britain has been running this experiment for thirty years. The results are consistent.

The harder objection

The most uncomfortable challenge to this argument is the jobs one. AI is changing work across entire sectors. The disruption is coming whether or not Britain produces the companies driving it. A Britain with no domestic AI industry is not protected from those changes. It simply loses the tax revenues, the wages, and the new companies that a domestic industry generates alongside the disruption it causes. The founders who leave take the upside with them. The disruption arrives regardless.

The fourth chapter describes what the escape actually requires, and why the window for it is shorter than most people realise.

CHAPTER FOUR

The Escape

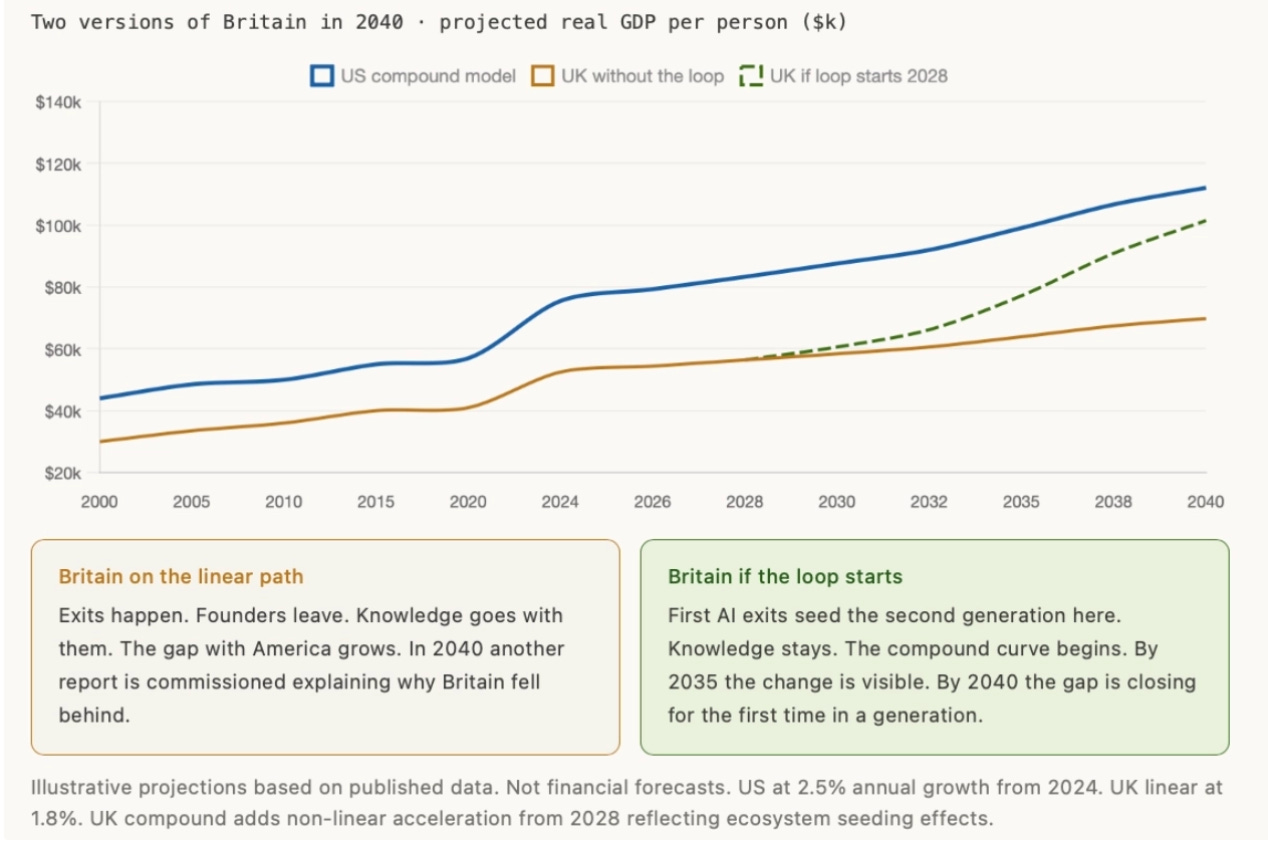

Picture two versions of Britain in 2040.

In the first, the AI companies being built in London and Cambridge and Bristol today produced their first significant exits between 2028 and 2033. Several of the founders who built them were persuaded to stay. Not by a summit or a press release, but by a specific set of signals that Britain sent between 2026 and 2030. Those founders recycled their exits into the next generation of British AI companies, bringing with them the hard-won knowledge of what it actually takes to build something at scale. By 2040 the loop has been running for roughly a decade. The ecosystem is not Silicon Valley. But it is self-sustaining, growing faster than every other part of the British economy, and closing the gap with America at a rate that would have seemed impossible in 2025.

In the second, the exits happened on the same schedule but the signals were never sent clearly enough, or were reversed by the budget that followed the one that introduced them. The founders who might have stayed did the arithmetic and concluded that a country whose rules shift with every political cycle was not worth building inside for thirty years. The loop never started. By 2040 Britain is still producing world-class research, still training exceptional engineers, still generating the ideas that other countries grow into industries. The gap with America, already twenty-three thousand dollars per person in 2024, is wider. Another report is commissioned to explain the failure. It reaches the same conclusions as the Draghi report of 2024, with an additional decade of evidence.

The difference is determined by the accumulation of decisions made between now and approximately 2030.

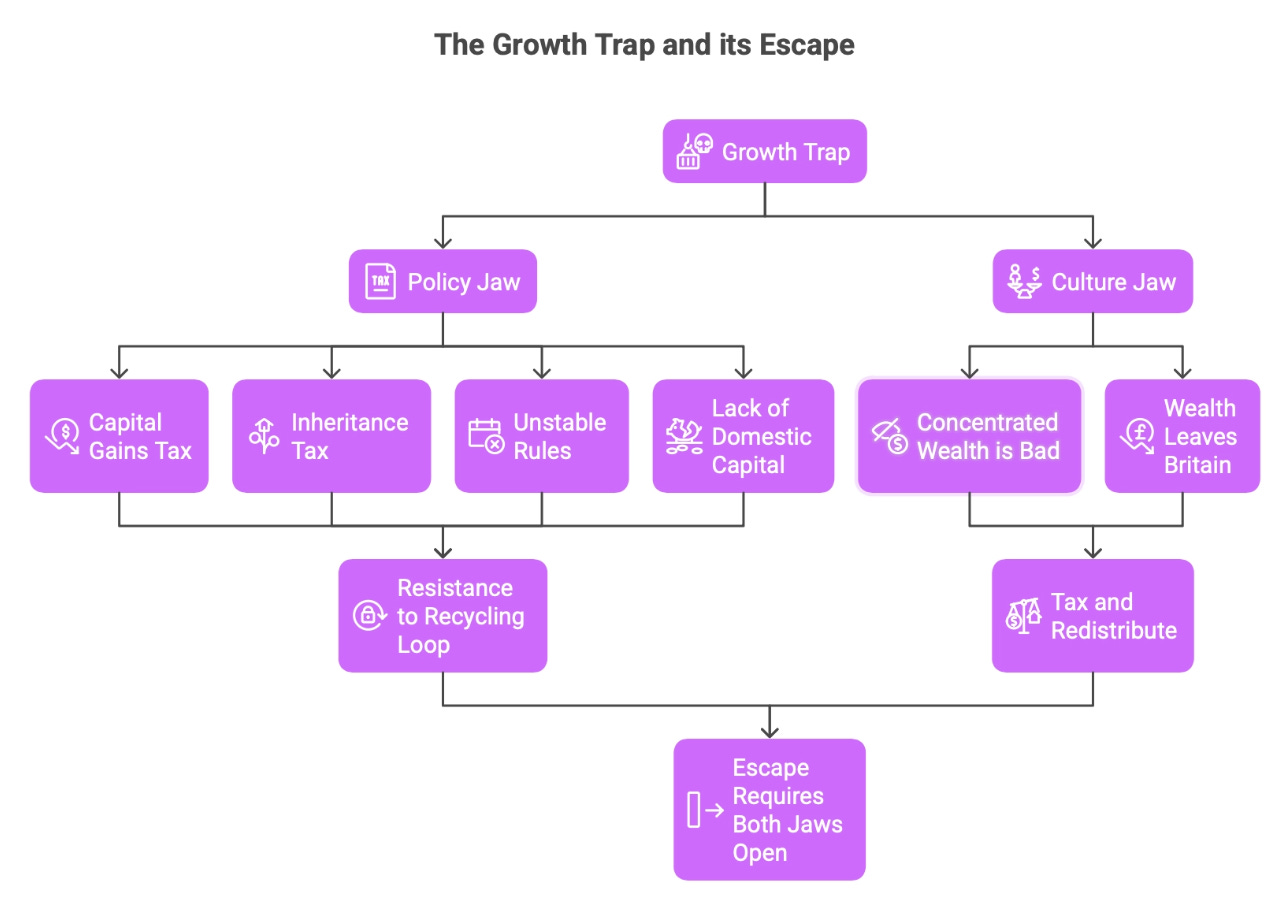

The trap has two jaws

The Growth Trap that holds Britain in slow linear growth has two jaws that work together, and both must open simultaneously for the escape to work.

The first jaw is policy. The combination of how capital gains are taxed on founder exits, how inheritance tax applies to operating businesses, how unstable the rules have become across successive budgets, and how little domestic capital exists at frontier scale, has made Britain resistant to the recycling loop. Not by design, but through the slow build-up of individually defensible decisions that nobody has assessed together for their combined effect.

The second jaw is culture. Britain has a story about wealth that it tells itself with great consistency: that concentrated wealth is evidence of a system that has failed, and the right response is to tax it and redistribute it. Those values are not the problem. The problem is applying them without distinguishing between wealth that stays and compounds inside Britain and wealth that simply leaves.

Change the policy without changing the culture and the culture finds ways to reverse the policy at the next election. Change the culture without changing the policy and the founders who are persuaded to stay still leave because the numbers do not work.

The signal

Herman Narula said explicitly before he left that the current rates were not the breaking point. The instability was. A country that changes its capital gains treatment for founders three times in a decade, that introduces and then removes relief for entrepreneurial assets, that threatens exit taxes and then retreats, is telling every founder something specific about the reliability of the environment in which they are being asked to make thirty-year bets.

Three things would change that signal. A statutory commitment, with cross-party support, that the core framework for technology founders will not change for ten years. A restoration of a genuinely preferential capital gains rate for founders who have built operating companies over many years - not traders, not passive investors - with a residency requirement so that gains stay inside the ecosystem. And the removal of inheritance tax from operating businesses where the founder is still actively building, because a forty percent tax levied at death catches the builders, not the inheritors.

In near-term revenue terms the cost of all three is close to nothing. The cost is political capital, which is why they have not happened.

The capital

Britain has one of the largest pools of long-term institutional capital in the world. Almost none of it flows into the British technology ecosystem at frontier scale. The average British pension fund is more likely to hold Apple, Microsoft, or Nvidia than the British AI company that might become their equivalent in thirty years.

The parallel requirement is a London Stock Exchange that is genuinely competitive with Nasdaq. ARM chose Nasdaq. Wise moved to New York. Revolut is being lobbied to consider London as a secondary option. The specific reasons - stamp duty on transactions, lower liquidity, slower index entry, lower valuations for growth companies - are all addressable. Every one of them is a political decision, not a technical problem.

The architecture

A data centre that takes four years to approve in Britain takes eighteen months elsewhere. Faster approval of the power generation and grid capacity that an AI economy requires is not a technology policy in itself. It is the condition on which technology policy can work at all. And a government that uses artificial intelligence to reform its own processes - faster planning decisions, faster visa processing, faster regulatory approvals - tells its founders something important: that it understands the technology seriously enough to stake its own credibility on it.

The twenty

The companies that could produce Britain’s founding cohort of AI recyclers are being built right now. Wayve is running Uber robotaxi trials in London in 2026. Isomorphic Labs, founded by Demis Hassabis and spun out of DeepMind, raised $600 million and is preparing to launch the first AI-designed drug trials. Nscale raised $1.1 billion to build AI infrastructure on renewable energy. Quantexa reached a $2.6 billion valuation. Synthesia reached a $2.1 billion valuation with hundreds of Fortune 500 companies as customers. Luminance is deploying proprietary legal AI across seventy countries. Cera delivers over sixty thousand AI-powered home healthcare appointments daily. CMR Surgical has raised over $600 million to build robotic surgery systems across Europe and Asia.

Each could produce a founder with the capital and operational knowledge to seed the next generation. Whether they do depends entirely on whether Britain has created the conditions that make staying preferable to leaving.

PayPal’s loop started with fewer than twenty recyclers. Britain needs enough density that a founder looking for capital and hard-won operational experience can find both without boarding a plane.

What the maths shows

Britain’s GDP is three trillion pounds. Growing at five percent annually for a decade means adding roughly one hundred and eleven billion pounds of new economic activity every year.

Twenty founders, each building a company worth a billion pounds and keeping seven percent, produce twenty companies worth fourteen billion pounds each. The total equity value created is two hundred and eighty billion pounds. But the wages those companies paid, the taxes they generated, the customer value they created, the ecosystem their exits seed - the total flowing outward to ordinary people is multiples of the equity figure alone. One generation of exits does not close a thirty-three-thousand-dollar gap. The loop does. Those exits seed the next generation of companies, which seed the generation after, each cycle starting from a larger base than the last. That compounding is what the five percent requires. Twenty founders gets you there for one year. The loop gets you there every year after that.

Five percent GDP growth requires not a debate about whether the wealthy deserve sympathy. It requires a decision about whether Britain would rather tax the exits it has or compound the exits it could have. The two are not the same choice. Britain has been treating them as if they were for twenty-five years.

The bill is a twenty-three-thousand-dollar gap per person per year. It is the nurse who cannot afford the house. It is the school underfunded by a Treasury that redistributed gains Britain did not generate.

The window

The PayPal exit was October 2002. Founders Fund opened in 2005. Three years separated the origin exit from the seeding of the second generation, and in those three years the architecture of the Silicon Valley compound loop was set.

Britain’s equivalent window is 2027 to 2032. Five years in which the decisions of a small number of people will determine the shape of the British technology economy for the following thirty years. The country that acts before the evidence is conclusive benefits from the compounding. The country that waits for the evidence commissions the report explaining why it fell behind.

Britain has been commissioning those reports for twenty-five years.

What will it actually take to make the next one stay?

Born Here, Grown Elsewhere examines Britain’s technology economy and the Growth Trap that prevents British-created value from compounding inside Britain. The Growth Trap framework identifies two simultaneous causes: policy choices that discourage founder reinvestment, and cultural beliefs that treat wealth creation as extraction rather than as national infrastructure. Both jaws must open simultaneously for the escape to work. The framework applies wherever compounding is blocked by simultaneous structural and cultural resistance - in national economies, in companies, in cities, and in the decisions of individuals.

A NOTE ON SOURCES AND METHOD

Income figures throughout come from World Bank and IMF purchasing power parity data. The technology sector attribution draws on ITIF research, BEA digital economy data, and LSE productivity analysis. The non-technology baseline figures are estimates derived from published data ranges rather than a single citable source; they are directionally consistent with ITIF and BEA research and should be read as approximations rather than precise calculations. Company valuations reflect figures available at the time of writing in March 2026. All GDP projections in Chapter Four are illustrative models built from published data ranges, not financial forecasts. All quotes attributed to named individuals are drawn from published interviews and public testimony cited in the bibliography below.

BIBLIOGRAPHY AND FURTHER READING

Income and GDP data

World Bank. GDP per capita, PPP (current international dollars). World Development Indicators. data.worldbank.org

International Monetary Fund. World Economic Outlook Database. October 2024 and April 2025 editions. imf.org

Office for National Statistics. GDP first quarterly estimate, UK: October to December 2025. February 2026. ons.gov.uk

Office for Budget Responsibility. Economic and fiscal outlook. March 2026. obr.uk

House of Commons Library. Gross domestic product (GDP): Economic indicators. March 2026. commonslibrary.parliament.uk

Technology sector attribution

Information Technology and Innovation Foundation. “Six Tech Industries Accounted for More Than One-Third of GDP Growth in the Last Decade.” May 2023. itif.org

Bureau of Economic Analysis. Measuring the Digital Economy. 2022. bea.gov

The Draghi Report and European competitiveness

Draghi, Mario. The Future of European Competitiveness. European Commission. September 2024. commission.europa.eu

Capital gains tax

House of Commons Library. Capital gains tax: recent developments. March 2026. commonslibrary.parliament.uk

HM Revenue and Customs. Capital Gains Tax: rates of tax. November 2024. gov.uk

The PayPal ecosystem

Soni, Jimmy. The Founders: The Story of PayPal and the Entrepreneurs Who Shaped Silicon Valley. Simon and Schuster. 2022.

SEC. “eBay Completes PayPal Acquisition.” October 2002. sec.gov

British technology losses and the millionaire exodus

TechCrunch. “SoftBank acquires UK AI chipmaker Graphcore.” July 2024. techcrunch.com

Wikipedia. “Arm Holdings.” Accessed March 2026.

Wikipedia. “Google DeepMind.” Accessed March 2026.

Henley and Partners. Private Wealth Migration Report 2025. henleyglobal.com

Witness testimony

Hauser, Hermann. Twitter, July 2016. twitter.com/hermannhauser

Hauser, Hermann. Interview with Cambridge Independent. August 2020. cambridgeindependent.co.uk

Hauser, Hermann. Interview with UK Tech News. June 2022. uktech.news

Hussey-Yeo, Barney. Evidence to House of Lords Communications and Digital Committee. November 2024. parliament.uk

Hussey-Yeo, Barney. Interview with CNBC. October 2024. cnbc.com

Hussey-Yeo, Barney. “UK tech’s problem isn’t taxes - it’s ambition.” Fortune. November 2024. fortune.com

Narula, Herman. “Tech entrepreneur Herman Narula: Why I’m swapping UK for UAE.” The National. November 2025. thenationalnews.com

Narula, Herman. Interview with The Telegraph. November 2025.

Revolut and British AI champions

Tech Nation. UK AI Sector Spotlight 2025. technation.io

The Tech Founders. “Top 100 UK AI Startup Investments in 2025.” thetechfounders.co.uk

Further reading

Thiel, Peter and Masters, Blake. Zero to One: Notes on Startups, or How to Build the Future. Crown Business. 2014.

Draghi, Mario. The Future of European Competitiveness: A Competitiveness Strategy for Europe. European Commission. September 2024.

Lacy, Sarah. Once You’re Lucky, Twice You’re Good: The Rebirth of Silicon Valley and the Rise of Web 2.0. Gotham Books. 2008.

Roelof Botha, various talks on the Sequoia model of patient, compounding capital. Sequoia Capital podcast archive and YouTube.

The Xeme Framework: Aditya Sehgal Xeme Framework

Check out some of my other Frameworks on the Fast Frameworks Substack:

The Decision Framework: DECIDE

The Alpha Engine Framework for Venture & Angel Investing

Don’t Hire an Agency. Build a Memetic Engine - The memetic engine framework

Fast Frameworks AI Tools: Cortex

The Exponential AI Adoption Framework

Moltbook and the Entity AI Framework

May every sunset bring you peace!

Entity AI, swarms and the future of work (Asymmetric Podcast)

Fast Frameworks Podcast: Entity AI-Episode 8: Meaning, Mortality, and Machine Faith

Fast Frameworks Podcast: Entity AI - Episode 7: Living Inside the System

Fast Frameworks Podcast: Entity AI – Episode 5: The Self in the Age of Entity AI

Fast Frameworks Podcast: Entity AI – Episode 4: Risks, Rules & Revolutions

Fast Frameworks Podcast: Entity AI – Episode 3: The Builders and Their Blueprints

Fast Frameworks Podcast: Entity AI – Episode 2: The World of Entities

Fast Frameworks Podcast: Entity AI – Episode 1: The Age of Voices Has Begun

The Entity AI Framework [Part 1]

The Promotion Flywheel Framework

The Immortality Stack Framework

Frameworks for business growth

The AI implementation pyramid framework for business

A New Year Wish: eBook with consolidated Frameworks for Fulfilment

AI Giveaways Series Part 4: Meet Your AI Lawyer. Draft a contract in under a minute.

AI Giveaways Series Part 3: Create Sophisticated Presentations in Under 2 Minutes

AI Giveaways Series Part 2: Create Compelling Visuals from Text in 30 Seconds

AI Giveaways Series Part 1: Build a Website for Free in 90 Seconds

Business organisation frameworks

The delayed gratification framework for intelligent investing

The Fast Frameworks eBook+ Podcast: High-Impact Negotiation Frameworks Part 2-5

The Fast Frameworks eBook+ Podcast: High-Impact Negotiation Frameworks Part 1

Fast Frameworks: A.I. Tools - NotebookLM

The triple filter speech framework

High-Impact Negotiation Frameworks: 5/5 - pressure and unethical tactics

High-impact negotiation frameworks 4/5 - end-stage tactics

High-impact negotiation frameworks 3/5 - middle-stage tactics

High-impact negotiation frameworks 2/5 - early-stage tactics

High-impact negotiation frameworks 1/5 - Negotiating principles

Milestone 53 - reflections on completing 66% of the journey

The exponential growth framework

Fast Frameworks: A.I. Tools - Chatbots

Video: A.I. Frameworks by Aditya Sehgal

The job satisfaction framework

Fast Frameworks - A.I. Tools - Suno.AI

The Set Point Framework for Habit Change

The Plants Vs Buildings Framework

Spatial computing - a game changer with the Vision Pro

The ‘magic’ Framework for unfair advantage