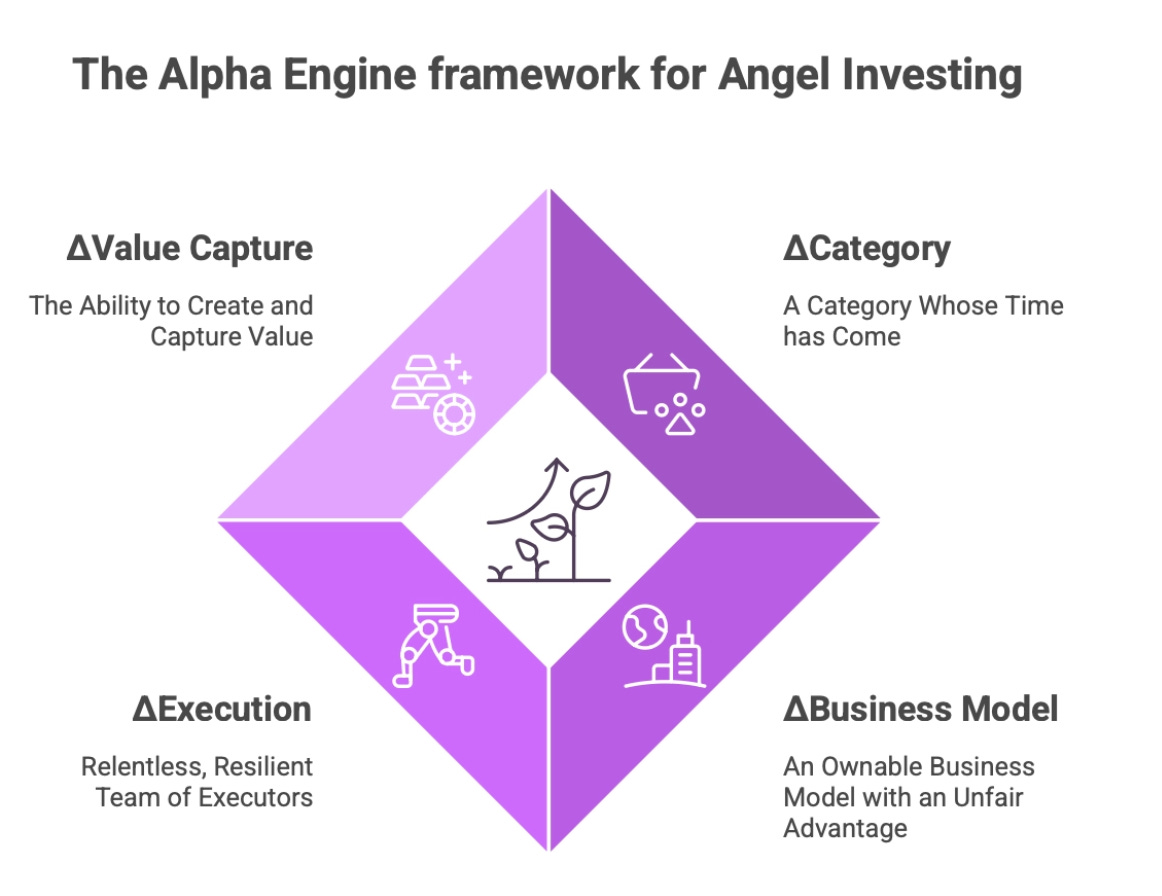

The Alpha Engine Framework for Venture & Angel Investing

Test Your Story if You're Raising. Check Your Assumptions if You're Investing. Use the Alpha Engine GPT.

Every venture investor has a story about the one that got away. The deal they saw early, liked, and passed on, only to watch it become a billion-dollar company from the sidelines. When you ask them what went wrong, the answer is almost always the same: they got one dimension right and missed another. They loved the founder but doubted the market. They believed in the market but could not see how the business model would scale. They liked everything about the company but had nothing to offer it beyond a cheque.

Venture outcomes are not built on one thing going right. They are built on four things going right simultaneously. And the relationship between those four things is not additive. It is multiplicative. That distinction changes everything.

The Framework Formula: Four Deltas

Each delta represents a dimension of uplift. Category is the wave the company is riding. Business Model is how the company converts that wave into durable advantage. Execution is the team’s ability to build, adapt, and endure. Value Capture is the investor’s lever: it combines what you contribute to the company (improving probability of success) and how you structure the deal (improving your payout when that success arrives).

The multiplication sign is the most important element in the equation. In an additive model, strength in one area compensates for weakness in another. In a multiplicative model, it does not. A brilliant team in a dead category produces nothing: 2 × 0 × 1.5 × 1.5 = 0. A booming category with a broken business model burns cash spectacularly: 2 × 0 × 1.5 × 1.5 = 0. A strong company backed by a passive investor who overpaid grows nicely and still returns mediocre multiples.

Conversely, even modest advantages across all four dimensions compound dramatically. If each delta scores 1.5 (not exceptional, just meaningfully above average) the total is 1.5 × 1.5 × 1.5 × 1.5 ≈ 5×. A 50% edge on each lever produces a 5× outcome. In my Hyper Growth Framework, I demonstrate this same principle applied to business operations: improving each of four revenue variables by just 10% produces nearly 50% total growth. The Alpha Engine applies the identical logic to investing decisions. The maths of multiplication rewards breadth of advantage over depth in any single dimension.

I have also built The Alpha Engine as an interactive GPT that walks you through all four deltas on a live deal. Upload a pitch deck, answer its questions, and it scores the opportunity. Link at the end of this piece.

What Zero Looks Like

“Zero in any dimension collapses everything” is not rhetoric. It is a practical filter. But nothing is literally zero, so here is what zero means in practice:

Category zero: the market is flat or shrinking, or the timing is wrong enough that the company will exhaust its capital before the wave arrives. No amount of execution compensates for a category that is not moving.

Business model zero: unit economics do not work even in the best-case cohort, or the differentiation is copyable in months. Growth exists but it is purchased, not structural, and it will stop the moment spending stops.

Execution zero: the founder cannot recruit, cannot ship, or cannot take feedback without breaking. The team has critical gaps with no plan to fill them.

Value capture zero: you cannot help, and you are paying a price where you need perfection from the other three levers just to break even. The deal structure offers no margin for error.

If you identify a genuine zero on any lever, stop. The other three do not matter.

Lever 1: A Category Whose Time Has Come

The starting point of venture investing is not the company. It is the category.

Most people evaluate startups the way they evaluate job candidates: they look at the individual and ask whether this person is impressive. Venture investing requires the opposite instinct. Look at the wave first. Ask whether this wave is big enough and fast enough that even a good-not-great surfer will have an extraordinary ride.

This is not an argument against founder quality. It is an argument about sequencing. Category selection comes first because it sets the ceiling. The best founder in a mature, slow-growing market will build a good business. The best founder in a category that is inflecting will build a transformative one. The category does not guarantee success, but it determines the scale of success that is possible.

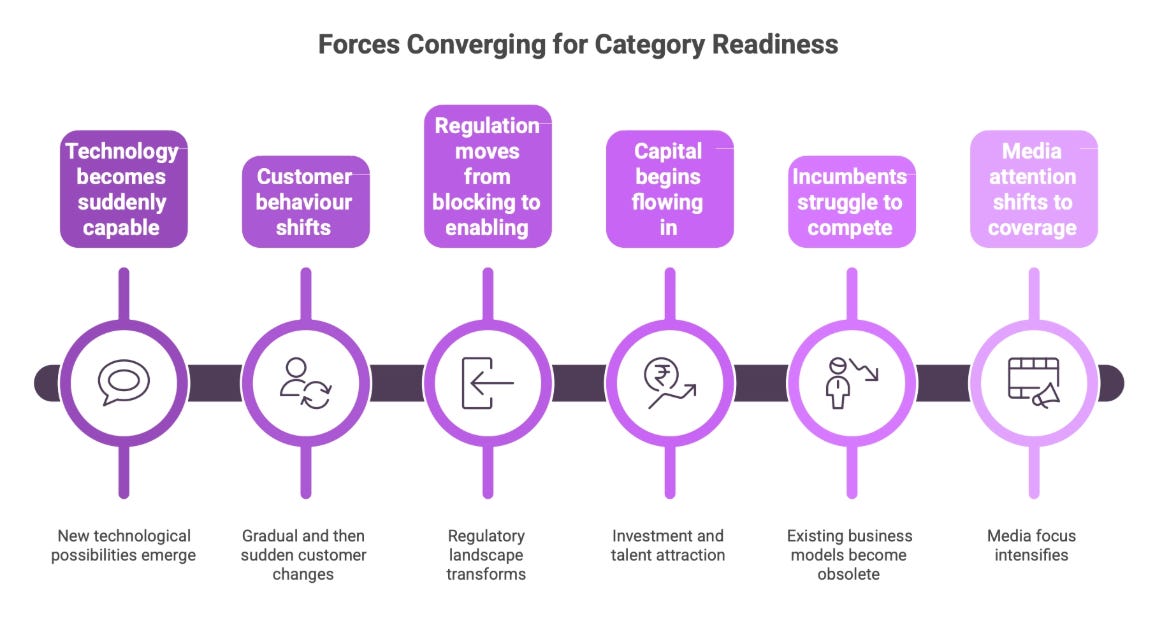

What makes a category ready? Several forces converge at once. Technology becomes suddenly capable of something previously impossible or prohibitively expensive. Customer behaviour shifts, often gradually, then all at once. Regulation moves from blocking to enabling, or creates disruption by changing the rules. Capital begins flowing in, which attracts talent, which accelerates development, which attracts more capital. Incumbents discover that their existing business models, distribution, or incentives actively prevent them from competing on the new dimension. Media attention shifts from scepticism to breathless coverage.

The useful test is not “is this a good category?” but “is this category accelerating right now, and will it still be accelerating in three to five years?” Look for leading signals: the best technical talent migrating into the space, early-adopter behaviour spreading to mainstream users, regulatory frameworks evolving, and founders you respect choosing to start companies here. If the smartest people you know are leaving comfortable positions to build in a category, the category is probably ready.

The Sub-Category Trap

A common mistake is evaluating categories at the wrong altitude. Broad categories like “healthcare” or “fintech” are too wide to be useful as investment theses. Within any large category, including ones that appear slow-growing in aggregate, there are sub-categories experiencing hypergrowth. Traditional grocery retail grows at low single digits. But the sub-category of personalised nutrition, sitting at the intersection of AI and health data, is inflecting. Insurance has been “boring” for decades. But the sub-category of parametric insurance, where payouts trigger automatically from data rather than claims, is growing at venture speed. The discipline is to identify the specific sub-category where the inflection is happening and to recognise that these pockets of hypergrowth are often where a new dimension of competition is emerging. In my Magic Framework, I describe how unfair advantage comes from competing on a dimension that does not yet exist in the eyes of incumbents, like an ant from a 3D world performing “magic” in Flatland. The best sub-categories to invest in are the ones where a new dimension is becoming relevant along an S-curve: early enough that incumbents are ignoring it, late enough that early adopters are proving it works.

Macro-Themes

Rather than evaluating categories in isolation, cluster them into macro-themes where your conviction runs deepest. Three natural clusters emerge from current inflection points.

Planet covers climate, sustainability, energy transition, circular economy, and environmental systems. In my Risk Framework, I describe climate change as the ultimate grey rhino: a highly probable, high-impact threat that humanity keeps watching from a comfortable distance. The investment implication is that the regulatory and consumer tailwinds here are generational, because the grey rhino is now close enough that governments and consumers are finally moving.

Life covers healthcare, nutrition, longevity, mental health, and ageing. Demographics and technology are converging to reshape how humans live longer and better.

Tech covers AI, infrastructure, robotics, decentralised systems, and digital networks. This is the enabling layer that accelerates everything else.

The discipline is focus. An investor that backs everything backs nothing. In my Innovation Framework, I describe how constraints force creativity. The same principle applies here: constraining your category focus forces deeper understanding, which produces better pattern recognition, which generates better deal flow. Category conviction creates gravity. Founders seek out investors who understand their world, because those investors add something beyond money.

The person betting on the wave will almost always outperform the person betting against it, no matter how talented the surfer.

Lever 2: An Ownable Business Model with Unfair Advantage

Category tailwinds get you into the game. The business model determines whether you win it.

The single question this lever answers is: what is the durable advantage, and is it showing up in behaviour?

The strongest business models are advantaged along a dimension of competition that appears secondary today but becomes decisive tomorrow. In my Magic Framework for Unfair Advantage, I describe this through the Flatland analogy: an ant from a 3D world appears to perform magic in a 2D world, because it operates on a dimension the Flatties cannot see. In venture investing, the most valuable companies are the ones competing on a dimension the rest of the market has not yet recognised as relevant. Amazon did not win retail on selection. It won on logistics infrastructure, a dimension nobody else took seriously until it was too late to replicate. Stripe did not win payments on price. It won on developer experience, a dimension the incumbents did not even recognise as competitive. Nvidia built deep architectural expertise in GPUs long before anyone understood that AI would make that expertise the most valuable capability in technology. In each case, the company invested heavily in a dimension that looked irrelevant, and then the market shifted to make that dimension the one that mattered most.

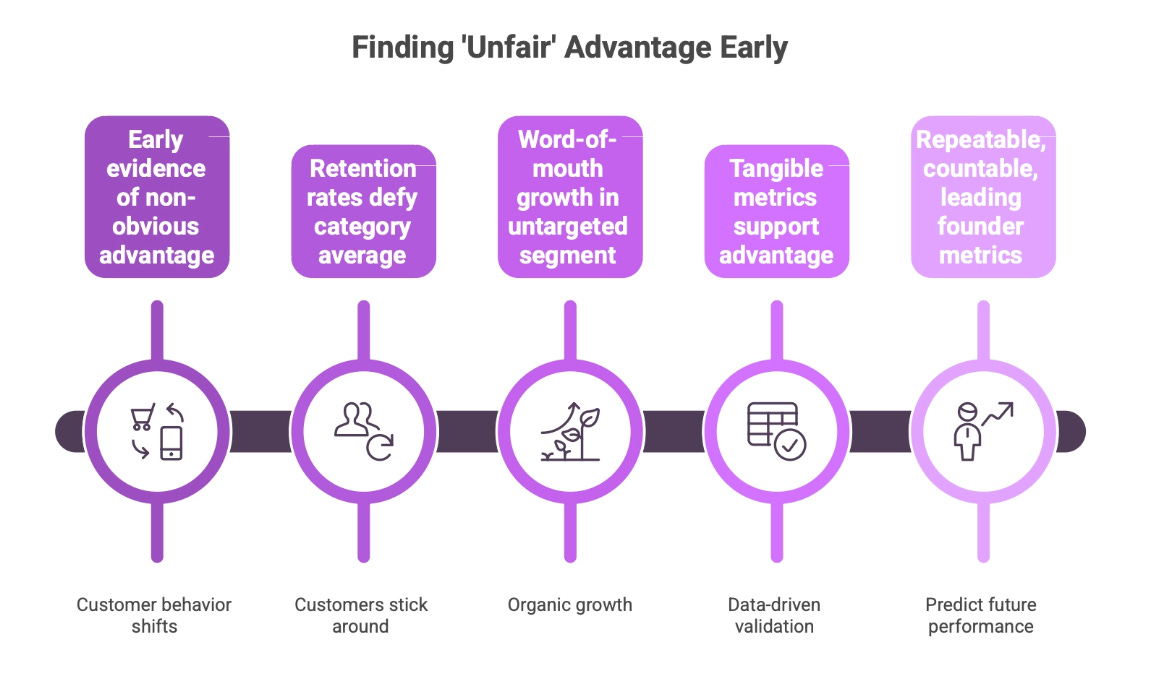

When evaluating a startup’s business model, look for proof of concept along their chosen dimension. Early evidence, even messy and incomplete, that the non-obvious advantage is beginning to matter. This is visible in customer behaviour before it shows up in market data. Customers doing unexpected things with the product. Retention rates that defy the category average. Word-of-mouth growth in a segment nobody targeted on purpose. The advantage must be tangible in the metrics, not just asserted in the pitch deck. Look for what I call founder metrics: numbers that are repeatable (not one-off wins), countable (with real data behind them), and leading (they predict future performance, not just describe the past).

The Behavioural Proof Layer

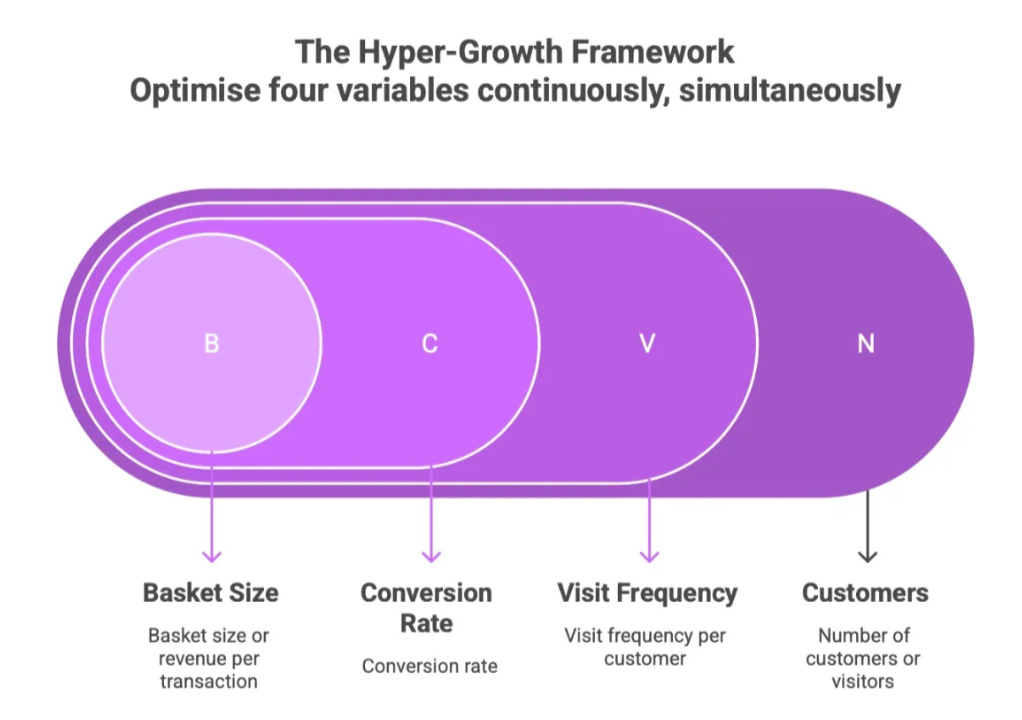

Growth claims need decomposition. In my Hyper Growth Framework, I break revenue into four multiplicative drivers:

Where N is the number of customers or visitors, V is visit frequency per customer, C is conversion rate, and B is basket size or revenue per transaction. Improving each by just 10% produces nearly 50% total growth, because the relationship is multiplicative. Improving each by 80% results in 10X growth.

The same decomposition reveals whether a startup’s growth is structural or purchased. The quick test: outperforming on one driver can be bought, two signals structural pull, three or four and you are looking at something with a genuine engine underneath. Many startups show impressive top-line growth driven entirely by N, funded by marketing spend. When that spend stops, growth collapses. If a company has both higher conversion and higher visit frequency than its competitors, something fundamental is working. If it only has higher visitor numbers because it is spending more on ads, nothing fundamental is working.

The Unit Economics Gate

Once you believe the advantage is real and the growth is structural, there is one final check: the Fixed Cost Principle. The core transaction must demonstrate unit-level profitability before large-scale expansion costs distort the picture. Prove that the unit works at small scale, then add the fixed costs of growth. If the unit economics do not work before you scale, they will not magically improve after. Scaling a money-losing unit just scales the losses.

The business model is not a spreadsheet. It is the reason the company will still be winning five years from now, even after competitors have seen exactly what it does.

Lever 3: Relentless, Resilient Executors + Team

Category and model are necessary conditions. The founding team is the sufficient condition.

Building a venture-scale company is a decade-long endurance test that selects for a very specific set of traits. Talent matters, but talent is common. What is uncommon is the combination of traits that allows people to sustain performance through years of uncertainty, rejection, near-death experiences, and the grinding monotony that sits between every breakthrough. The framework evaluates founders on character first, composition second, and credentials third.

Character

Character is the foundation. The founders must be passionate and purpose-driven: not opportunistically chasing a hot category, but drawn to the problem with genuine conviction that survives the first (and second, and fifth) moment when everything goes wrong. They must have skin in the game, with meaningful personal exposure that aligns their incentives with everyone else at the table. And they must be in it for the long term. Venture building is not a sprint. Founders who are mentally planning their exit at Series A will optimise for the wrong things at every decision point. You can feel this in a conversation. The founder who talks about the problem they are solving sounds different from the founder who talks about the exit multiple they are targeting.

Composition

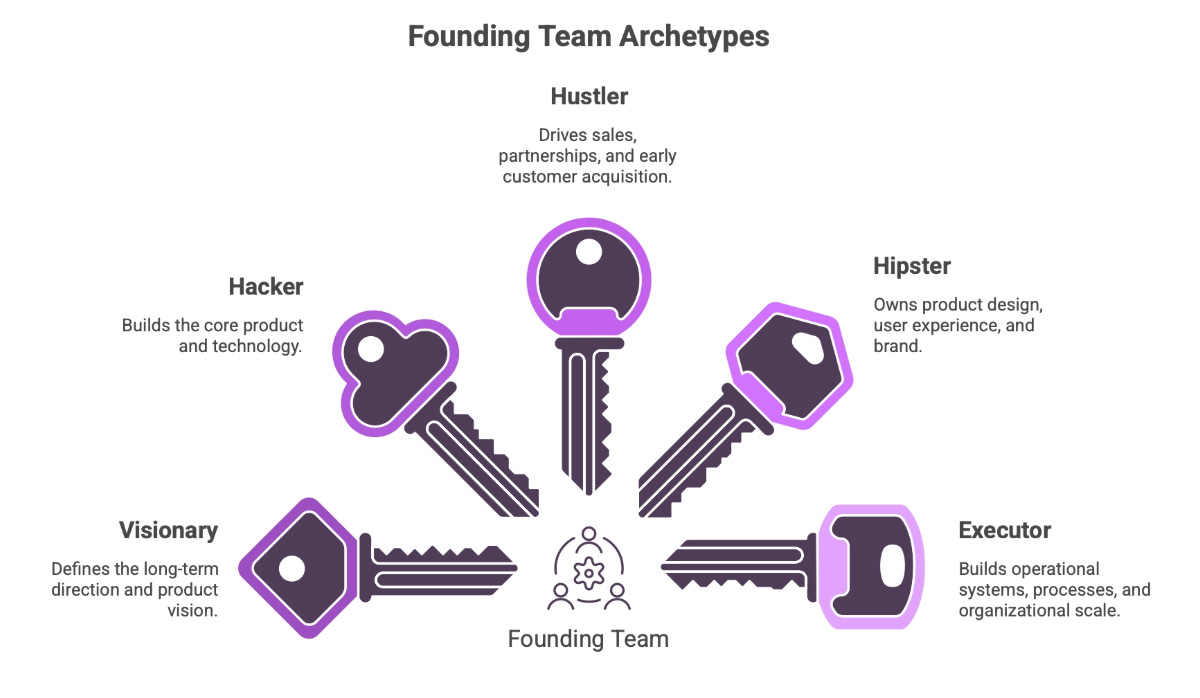

Composition matters because no single founder embodies everything a startup needs. In my Team Design Framework, I describe how the structure of your team becomes the structure of what you build, following Conway’s Law. The same principle applies to founding teams: a team heavy on vision but light on execution will build something beautiful that never ships. A team heavy on hustling but light on product thinking will ship something that nobody loves. A balanced founding team contains several archetypes, and the interplay between them determines how well the company navigates the full journey from idea to scale. The Visionary defines the long-term direction and product vision: where the company is going and why it matters. The Hacker is the technical architect building the core product and technology. The Hustlerdrives sales, partnerships, and early customer acquisition: the commercial engine. The Hipster owns product design, user experience, and brand: how the company feels to its users. The Executor builds operational systems, processes, and organisational scale: how the company actually works as it grows.

The question is not whether the founding team has all five. It is whether they cover enough of them, and whether they are self-aware about their gaps. A visionary-hacker pair who know they need a hustler and are actively looking for one is stronger than a team of three visionaries who think sales will take care of itself. The brutal question that turns composition from a personality quiz into an execution test: what critical job is missing right now, and what is the plan to cover it in the next six months? If the answer is vague, the gap is real and growing.

Credentials

Credentials come last, but they are not irrelevant. Three dimensions of prior experience create useful signal: startup experience (have they built before, and do they understand the emotional and operational reality of year three when the excitement has worn off?), industry knowledge (do they have deep domain understanding, or are they tourists who read a report and got excited?), and financial discipline (do they understand capital structure, unit economics, and the difference between revenue and value?). Existing VC backing is also a signal, not because other investors are always right, but because navigating the fundraising process is itself a test of persuasion, resilience, and the ability to tell a story that survives scrutiny.

Character sustains. Composition scales. Credentials signal. In that order.

Lever 4: The Ability to Create and Capture Value

The first three levers are about evaluating the investment. The fourth is about what you, as the investor, bring and how value is created. For a structured view, see my Value Creation Framework. This is the lever that separates venture capital from passive stock picking. If you are not actively improving the odds of the companies you back, you are not a venture investor. You are a gambler with a better address book.

Value Capture has two parts: improving probability (making the company more likely to succeed) and improving payout (structuring the deal so that success translates into returns). Both matter. An investor who helps a company grow but overpaid at entry will watch the value they created accrue to someone else. An investor who got a great deal but adds nothing will watch the company underperform the scenario their model assumed.

This lever operates differently depending on whether you are an angel investor or a venture fund manager. The mechanisms differ, but the principle is identical.

For the Angel Investor

Improving probability is personal and direct. You create value by opening your network: making the one introduction that changes the founder’s trajectory, connecting them to their first enterprise customer, or getting them in front of the right Series A investor when the time comes. In my Network Framework, I describe how relationships follow the same growth laws as everything else: transmission minus decay. An angel’s value is directly proportional to the quality of their network and their willingness to activate it. The best angels are not just cheque writers. They are nodes in a network that the founder could not otherwise access.

Angels also improve probability through mentorship and pattern recognition, particularly if they have operating experience in the founder’s category. A former CPG executive backing a D2C food brand can compress years of learning into a few conversations. A former CTO backing a technical founder can help them avoid architectural mistakes that would cost six months and half the runway.

Improving payout for angels requires equal discipline. Enter at fair valuations, because overpaying for a great company can still produce mediocre returns. Negotiate for information rights so you can monitor progress and make follow-on decisions. Secure pro-rata rights in future rounds where possible, because the ability to double down on winners is where angel returns are really made. Build your portfolio honestly: the power law means most returns come from one or two investments, so diversification and sizing matter more than any single deal’s terms.

For the Venture Fund Manager

Improving probability happens through five channels. Deal flow maximisation: the best deals come through networks, not cold inbound. Ecosystem connection: linking portfolio companies to each other, to customers, to talent, and to strategic partners creates compounding value that no individual company could generate alone. Active board participation: providing strategic guidance, governance discipline, and honest feedback during critical growth phases directly influences outcomes. Founder community building: hosting events, building databases of founders across categories, and creating gathering points turns the firm’s network into a platform. In my Network Framework, this is deliberate transmission engineering: increasing the rate at which introductions and recommendations flow through the firm’s ecosystem. And connections to the broader ecosystem: systematically linking portfolio companies to corporates, talent pipelines, distribution channels, and accelerators extends their reach beyond what they could achieve alone.

Improving payout for fund managers requires the same entry-price discipline as for angels, plus additional structural tools: ownership targets, reserves strategy for follow-on, and active portfolio management against the original thesis.

Whether you are an angel writing a single cheque or a fund manager deploying a portfolio, the portfolio management principle is the same: water the winners, sell the weeds.

In my Compounding Framework, I describe how the key shift from linear to exponential growth is reinvestment: feeding the output of each cycle back into the next. The same logic applies to a venture portfolio. The returns from your winners, whether capital, attention, introductions, or board time, should be reinvested into making those winners even stronger. This feels counterintuitive because your instinct is to spend time on the companies that are struggling. But the maths is clear. A company growing at 3× that you help grow at 4× creates far more value than a company declining at 0.5× that you slow to 0.7×.

The venture investor does not just pick winners. They make winners. And they structure the relationship so that when the winners win, the investor wins too.

The Compounding Effect

Because the model is multiplicative, the maths rewards consistency across dimensions far more than excellence in any single one.

An investor that scores 1.0 on every lever (average category, average business model, average team, average value-add) produces a 1× outcome: market returns. Unremarkable.

An investor that scores 2.0 on one lever and 1.0 on the other three produces 2×. Better, but still modest.

An investor that scores 1.5 across all four produces 1.5 × 1.5 × 1.5 × 1.5 ≈ 5×. No single lever is exceptional, but the compounding across dimensions is powerful.

And if any single lever drops to 0.5: 1.5 × 1.5 × 0.5 × 1.5 ≈ 1.7×. One weak dimension destroys the compounding. The model is as much a risk framework as it is a return framework. In my Risk Framework, I describe how danger multiplied by exposure creates the real risk profile. The same multiplicative logic applies here: a weakness on one lever does not just subtract from returns. It divides them.

This is why due diligence must be systematic across all four dimensions. It is tempting to fall in love with one lever, a charismatic founder, a massive market, a beautiful business model, and wave away the others. The formula does not allow it. The multiplication sign is unforgiving.

The Flywheel: How the Investor Compounds

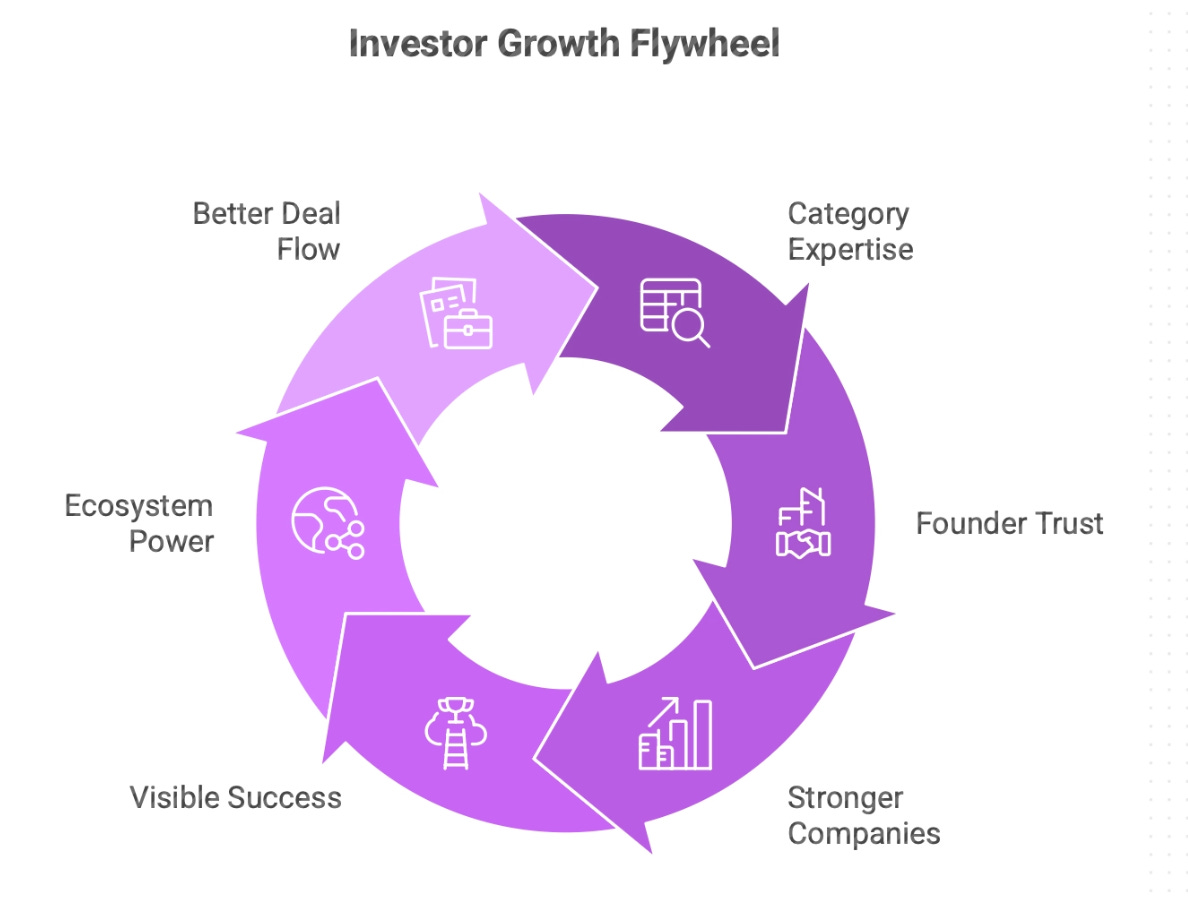

Lever 4 is deal-level: what you bring to a specific investment. The flywheel is career-level: how every deal you do makes the next one better.

The four levers describe how individual investments succeed. The flywheel describes how the investor themselves gets stronger over time. This applies equally to an angel building a personal brand and deal flow engine, and to a fund building institutional capability.

It starts with category expertise. The investor develops deep knowledge in their chosen themes. Not surface-level trend awareness, but genuine understanding of the technology, the customers, the competitive dynamics, and the regulatory landscape. In my Xeme Framework, I describe how real learning comes from experiential units I call xemes: you try something, the world pushes back, and you walk away knowing something you did not know before. Category expertise built from actual investments, board conversations, and founder relationships is made of xemes. Category expertise built from reading blog posts is not.

Category expertise attracts founders. Because the investor genuinely understands the space, the best founders seek them out first. They want investors who can challenge their assumptions, make useful introductions, and provide guidance that goes beyond generic advice. Deal flow quality improves.

Better founders build stronger companies. The combination of better selection (seeing the best deals) and active support (lever four) produces portfolio companies that outperform. The portfolio gets stronger.

Stronger companies generate visible success. Exits produce returns and reputation. Other founders notice. LPs notice (for fund managers) or co-investors notice (for angels). The investor’s brand grows not through marketing but through results. In my Network Framework, this is transmission at work: every successful outcome increases the rate at which people mention your name in rooms you are not in.

Visible success expands the ecosystem. The investor’s network deepens: founder communities, talent pipelines, corporate partnerships, co-investor relationships. Each new node in the network creates value for every other node.

A stronger ecosystem generates better deal flow. With reputation and network, the investor sees the best opportunities first, at better valuations, with stronger relationships. Which reinforces category expertise, because every new investment deepens understanding of the themes.

Category Expertise → Founder Trust → Stronger Companies → Visible Success → Ecosystem Power → Better Deal Flow → Category Expertise.

Each cycle through the flywheel strengthens the investor’s position. The advantage is cumulative and increasingly difficult for competitors to replicate. In my Compounding Framework, I describe how the key to exponential growth is never interrupting the compounding unnecessarily. The same principle applies to the venture flywheel: every cycle that completes makes the next cycle stronger. The investors who stay disciplined, same themes, same approach, same founder-first philosophy, for a decade or more build flywheels that spin faster with each rotation.

How AI Changes the Formula

AI is reshaping all four levers simultaneously, and the effects are not as simple as “everything gets better.”

Category selection becomes both easier and harder. AI tools can scan markets, analyse trends, and identify inflection points faster than any analyst. But everyone has access to the same tools, which means the obvious categories attract obvious capital. In my Exponential Growth Framework, I describe how S-curves move through phases: slow crawl, rapid ascent, plateau. AI compresses the time it takes for a category to become visible, which means the window between “interesting but unproven” and “obvious and overpriced” is shrinking. The edge shifts from identifying the category to understanding the specific sub-category where the inflection is happening, and understanding it deeply enough to distinguish the signal companies from the noise. This is where the Magic Framework becomes essential: the ability to see a new dimension of competition before the market recognises it cannot be automated, because by the time the dimension is visible to an algorithm, it is visible to everyone.

Business model evaluation becomes more rigorous at the surface level. AI can decompose the N × V × C × B equation in real time, benchmark against industry data, and flag structural weaknesses in unit economics before the second meeting. This is genuinely useful. It raises the floor of analysis quality across the industry. But it also means every investor is seeing the same red flags. The advantage shifts to understanding the non-obvious dimensions of competition, the Flatland-to-3D shift that the Magic Framework describes, which remain stubbornly resistant to algorithmic analysis. The question “on what dimension is this company building an advantage that nobody else recognises yet?” requires judgment, pattern recognition, and often a willingness to be wrong that AI cannot replicate.

Founder evaluation remains fundamentally human. AI can analyse a pitch deck, assess market size, and flag competitive risks. It cannot sit across a table from a founder and sense whether they will still be fighting in year seven when everything has gone wrong twice. Character, resilience, and team chemistry are felt, not computed. This is the lever where human judgment retains its greatest advantage. In my Xeme Framework, I describe how certain kinds of learning can only come from lived experience: you have to feel the pushback of reality to earn the knowledge. Evaluating founders is exactly this kind of knowledge. You build it over years of backing people, watching some succeed and others fail, and slowly developing the intuition to tell the difference.

Value creation and capture get amplified for those who are deliberate. AI tools allow investors to provide portfolio companies with capabilities that previously required large teams: market research, financial modelling, customer analysis, competitive intelligence, operational playbooks. An angel with AI tools can now provide the kind of strategic support that was once the exclusive domain of top-tier funds. A fund that builds AI-powered infrastructure for its portfolio creates a value-creation advantage that scales across every investment. But the risk is the same one I describe throughout my frameworks: AI makes activity look like progress. Sending a founder an AI-generated market report is not the same as sitting on their board and helping them make a hard decision. In my Pretotype Framework, I emphasise testing before building. The same applies here: use AI to test more hypotheses, analyse more data, and prepare more thoroughly. Do not use it to replace the conversations, the judgment calls, and the relationship-building that actually move the needle.

The real shift is this: AI compresses the time between “everyone can do basic analysis” and “only the best investors can see what the analysis misses.” The baseline of competence rises for everyone. The advantage moves entirely to judgment, relationships, and the willingness to commit to a thesis before the data makes it obvious. Those are human capabilities. They compound with experience. And they are exactly what the Alpha Engine’s four deltas are designed to evaluate.

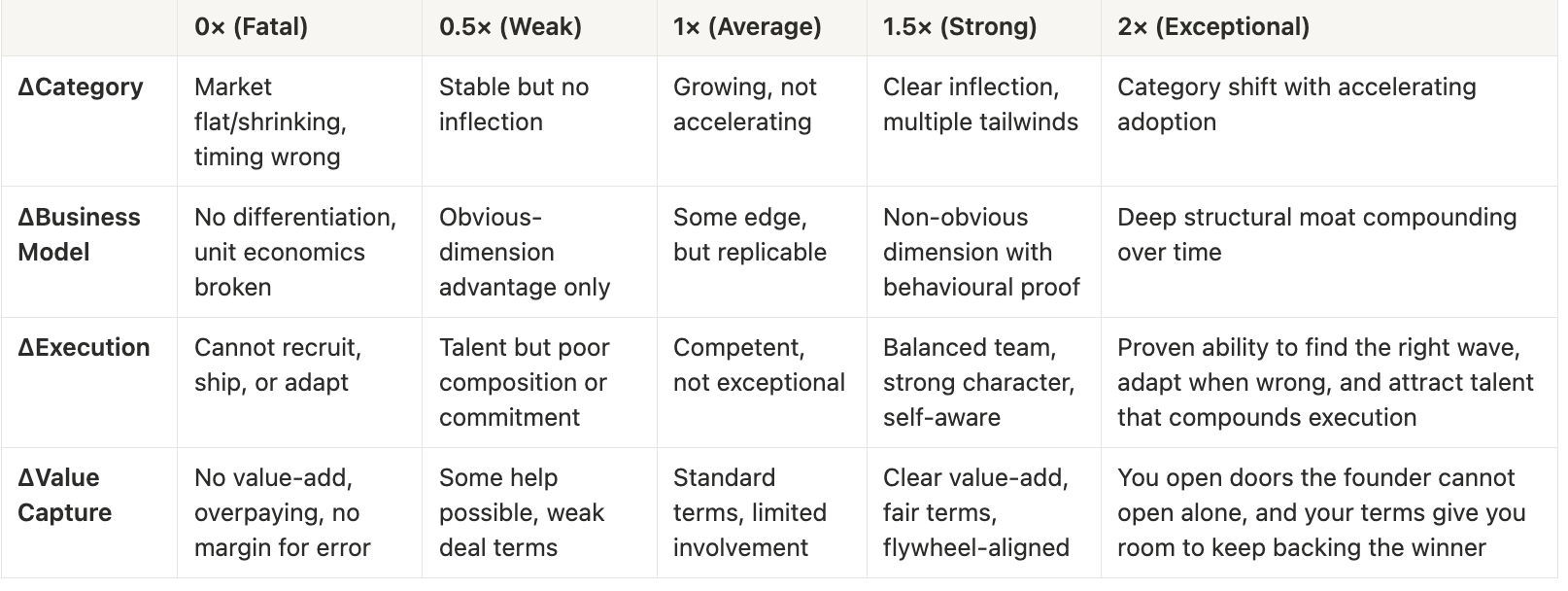

The Scoring Table

Key questions per lever:

ΔCategory: What is the exact sub-category, what tailwinds are structural not cyclical, and is timing inside the runway?

ΔBusiness Model: On what non-obvious dimension is advantage being built, how many of the four growth drivers outperform, and do unit economics work before scale?

ΔExecution: Is the founder purpose-driven or opportunity-chasing, what critical role is missing right now, and who owns filling it by when?

ΔValue Capture: What specific doors can you open that the founder cannot, is the entry price fair, and does this deal make your flywheel stronger?

Applications

For the angel investor evaluating a deal: Run every opportunity through the four deltas before you write the cheque. Score the category, the business model, the team (character, composition, credentials, in that order), and your own ability to help. The multiplication sign means you cannot compensate for a zero on any dimension. If you score the team as exceptional but the category as flat, the equation tells you to walk away, no matter how much you like the founder. That discipline is what separates angel investors who generate returns from those who collect interesting stories.

For the startup founder stress-testing your venture: Use the four deltas to evaluate yourself before investors do. Be honest about zeros and gaps. The multiplication sign is as unforgiving for you as it is for the people evaluating you, and they will see what you try to hide. Fix the weakest lever first, because that is where the multiplicative drag is greatest. A 0.5 on any lever halves your entire outcome.

For the VC fund evaluating investments: The four deltas provide a systematic first-pass filter that prevents the most common failure mode: falling in love with one lever and ignoring the others. Require the investment committee to explicitly rate all four before any decision. A 0.5 on any lever halves the expected outcome regardless of what the other three look like.

For founders raising capital: Use this framework to evaluate your investors, not just the other way around. Ask what they will actually do for you beyond writing the cheque. The best investors score high on all four levers. The worst score high on one and wave at the others. You are choosing a partner for a decade. Choose one who thinks in systems, not slogans.

Tooling - A custom GPT to use the Framework

I have built The Alpha Engine as an interactive GPT that applies this framework to real deals. Upload a pitch deck or describe an opportunity, and it will score each delta, calculate the multiplicative total, and show you what happens when the weakest lever moves up or down by half a point. It handles three personas: angel investors get diagnostic questions and an invest/pass/dig-deeper recommendation, startup founders get a strengths-and-weaknesses map with a fix-this-first priority, and VC funds get an IC-ready summary with scores, gaps, and follow-up questions.

Try The Alpha Engine GPT → here

Do not fall in love with the story. Protect the equation.

If you found this post valuable, please share it with your networks.

In case you would like me to share a framework for a specific issue which is not covered here, or if you would like to share a framework of your own with the community, please comment below or send me a message

CustomGPT built by asgardlabs.ai.

Check out some of my other Frameworks on the Fast Frameworks Substack:

Don’t Hire an Agency. Build a Memetic Engine - The memetic engine framework

Fast Frameworks AI Tools: Cortex

The Exponential AI Adoption Framework

Moltbook and the Entity AI Framework

May every sunset bring you peace!

Entity AI, swarms and the future of work (Asymmetric Podcast)

Fast Frameworks Podcast: Entity AI-Episode 8: Meaning, Mortality, and Machine Faith

Fast Frameworks Podcast: Entity AI - Episode 7: Living Inside the System

Fast Frameworks Podcast: Entity AI – Episode 5: The Self in the Age of Entity AI

Fast Frameworks Podcast: Entity AI – Episode 4: Risks, Rules & Revolutions

Fast Frameworks Podcast: Entity AI – Episode 3: The Builders and Their Blueprints

Fast Frameworks Podcast: Entity AI – Episode 2: The World of Entities

Fast Frameworks Podcast: Entity AI – Episode 1: The Age of Voices Has Begun

The Entity AI Framework [Part 1]

The Promotion Flywheel Framework

The Immortality Stack Framework

Frameworks for business growth

The AI implementation pyramid framework for business

A New Year Wish: eBook with consolidated Frameworks for Fulfilment

AI Giveaways Series Part 4: Meet Your AI Lawyer. Draft a contract in under a minute.

AI Giveaways Series Part 3: Create Sophisticated Presentations in Under 2 Minutes

AI Giveaways Series Part 2: Create Compelling Visuals from Text in 30 Seconds

AI Giveaways Series Part 1: Build a Website for Free in 90 Seconds

Business organisation frameworks

The delayed gratification framework for intelligent investing

The Fast Frameworks eBook+ Podcast: High-Impact Negotiation Frameworks Part 2-5

The Fast Frameworks eBook+ Podcast: High-Impact Negotiation Frameworks Part 1

Fast Frameworks: A.I. Tools - NotebookLM

The triple filter speech framework

High-Impact Negotiation Frameworks: 5/5 - pressure and unethical tactics

High-impact negotiation frameworks 4/5 - end-stage tactics

High-impact negotiation frameworks 3/5 - middle-stage tactics

High-impact negotiation frameworks 2/5 - early-stage tactics

High-impact negotiation frameworks 1/5 - Negotiating principles

Milestone 53 - reflections on completing 66% of the journey

The exponential growth framework

Fast Frameworks: A.I. Tools - Chatbots

Video: A.I. Frameworks by Aditya Sehgal

The job satisfaction framework

Fast Frameworks - A.I. Tools - Suno.AI

The Set Point Framework for Habit Change

The Plants Vs Buildings Framework

Spatial computing - a game changer with the Vision Pro

The ‘magic’ Framework for unfair advantage